The Fed’s Bond Diet

Bond investors may revisit an early catalyst to bond market weakness in 2013, when Federal Reserve (Fed) policymakers reconvene this week. The official statement following the conclusion of this Wednesday’s Fed meeting will be scrutinized for clues about whether the Fed’s bond appetite may be satiated. Minutes of the December 2012 Fed meeting, released during the first week of January, sparked selling among high-quality bonds, as investors feared the Fed would end or curtail bond purchases earlier than expected. Minutes also revealed that…”Several others thought that it would probably be appropriate to slow or to stop purchases well before the end of 2013, citing concerns about financial stability or the size of the balance sheet.” As we commented in early January, we believe bond market reaction to the Fed meeting minutes was overdone (please see the January 8, 2013, Bond Market Perspectives: Sour Start to New Year for more details), but scrutiny over the Fed’s bond holdings will continue.

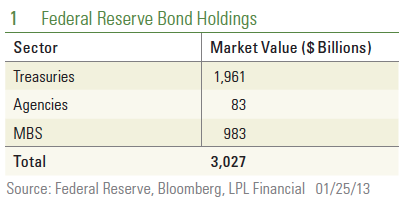

With the Fed’s balance sheet surpassing $3 trillion [Figure 1], investors’ attention may once again be drawn to the Fed’s bond buying. The Fed is widely expected to maintain its current bond-buying diet of $45 billion in long-term Treasuries and $40 billion of government-agency mortgage-backed securities (MBS) as Fed policymakers reconvene this week.

However, in 2013, the Fed is no longer offsetting Treasury purchases with Treasury sales. The Fed will be buying a total of approximately $115 billion of government bonds per month after including reinvestment flows, which have averaged slightly more than $30 billion per month over the last six months. At that rate, the Fed’s balance sheet will be steadily progressing toward $4 trillion, and bond investors are assessing the potential impact.

Fed Buying and Bond Valuations

Fed bond purchases, and subsequent expansion of the balance sheet, are one of the main drivers of expensive bond valuations. As the Fed’s balance sheet has grown with bond holdings, the yield on Treasury Inflation Protected Securities (TIPS) fell and, until recently, declined further into negative territory [Figure 2]. Fed bond purchases, in addition to their commitment to refrain from raising interest rates for an extended period have both contributed to making Treasury bonds expensive.

Fed bond purchases, and subsequent expansion of the balance sheet, are one of the main drivers of expensive bond valuations. As the Fed’s balance sheet has grown with bond holdings, the yield on Treasury Inflation Protected Securities (TIPS) fell and, until recently, declined further into negative territory [Figure 2]. Fed bond purchases, in addition to their commitment to refrain from raising interest rates for an extended period have both contributed to making Treasury bonds expensive.

Aside from the impact on valuations, the interest rate sensitivity of the Fed’s bond portfolio will continue to increase. Bond investors will monitor interest rate sensitivity, since it may influence the Fed’s decision on whether to continue buying bonds and at what pace. And so will Fed officials, as this week’s Weekly Economic Commentary notes: “…both the efficacy and the costs would need to be carefully monitored and taken into account in determining the size pace and composition of asset purchases” according to the Fed.

Our analysis of Fed bond holdings reveals an average coupon rate of 3.9% and average duration (a measure of interest rate sensitivity) of 6.5 years. As a rough rule of thumb, duration reveals the percentage change in a portfolio for a given change in interest rates. For example, if interest rates rise by 1%, the Fed’s portfolio would suffer a 6.5% loss in price. However, duration does not factor in time horizon. Should the 1% rise in interest rates occur over one year, the 6.5% loss would be offset by 3.9% of interest income for a net loss of 2.6%. Nonetheless, a 2.6% loss on the Fed’s $2.8 trillion market value of bond holdings produces a $74 billion loss.

According to Fed data, the Fed has an unrealized gain of $249 billion from its bond holdings. The unrealized gain suggests the Fed’s bond portfolio could, simplistically, sustain a 2% rise in interest rates (~$150 billion loss) before the Fed may come under political pressure to stop bond purchases. Over time, the Fed’s portfolio will change and market sensitivity will increase, making it hard to pinpoint how large an interest increase the Fed would be willing to suffer through. Adding more bonds in the coming months will add interest rate risk and increase the potential for loss in a rising rate environment.

All of this is not lost on the Fed officials, of course, and a working paper reveals that the Fed has already begun more thorough analysis of potential market impacts to its bond holdings over a longer term horizon. The Fed analyzed potential impacts under two policy paths: continuing the current pace of bond purchase through June 2013, and continuing purchases through the end of 2013. The Fed then subjected each path to: 1) a base case gradual rise in interest rates; 2) interest rates rise by 1% more than expected in the base case; and 3) a 1% decline in interest rates from the base case. The Fed also modeled assumptions for the pace of bond sells, pace of economic growth, and shape of the yield curve — all of which would impact bond prices. Many variables could affect the ultimate outcome, but the analysis is instructive of potential costs and risks faced by the Fed.

In summary, the Fed analysis found:

- Under the base case, the analysis revealed Fed losses would reach approximately $10 billion if purchases ended mid-year 2013, and $40 billion if purchases continued at the current pace through year-end 2013.

- Under the bear case where the interest rate increase is greater, the analysis revealed that losses peak at $60 billion if purchases ended mid-year 2013, and $125 billion if purchases continued at the current pace through year-end 2013.

The key takeaway is that there is a notable reduction in risk, according to the Fed’s analysis, if the Fed ends bond purchases before the end of 2013. Therefore, investors will continue to look for clues for an earlier-than-expected end to purchases.

Our view is that the end of bond purchases may not necessarily lead to a bond bear market. As stated in our January 8, 2013 Bond Market Perspectives, prior halts of Fed bond purchases have led to lower Treasury yields. Our concern relates to more economically sensitive, higher yielding segments of the bond market such as high-yield bonds that have benefited in part from increased demand from Fed bond purchases and policy that helped push high-quality bond yields extremely low. Given the strong start to the year by corporate bonds and other credit-sensitive sectors, a change in underlying market dynamics, such as Fed purchases, is that much more important. We are unlikely to get additional clarity from the Fed this week, which means investors may have to wait a few weeks before minutes are released and details on the latest Fed thoughts on bond purchases may become clearer. In the meantime, we continue to favor corporate bond sectors in fixed income portfolios and their greater yields as defense against rising interest rates. However, we remain watchful of a signal from the Fed that buying habits may change and warrant a reduction given now-higher valuations.

__________________________________________________________________________________________________________________________________________

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results. All indexes are unmanaged and cannot be invested into directly.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values and yields will decline as interest rates rise, and bonds are subject to availability and change in price.

Corporate bonds are considered higher risk than government bonds but normally offer a higher yield and are subject to market, interest rate and credit risk as well as additional risks based on the quality of issuer coupon rate, price, yield, maturity and redemption features.

Government bonds and Treasury Bills are guaranteed by the U.S. government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value. However, the value of fund shares is not guaranteed and will fluctuate.

High-yield/junk bonds (grade BB or below) are not investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

Treasuries are marketable, fixed-interest U.S. government debt securities. Treasury bonds make interest payments semi-annually, and the income that holders receive is only taxed at the federal level.

Treasury inflation-protected securities (TIPS) help eliminate inflation risk to your portfolio, as the principal is adjusted semiannually for inflation based on the Consumer Price Index—while providing a real rate of return guaranteed by the U.S. government.

Mortgage Backed Securities are subject to credit, default, prepayment risk that acts much like call risk when you get your principal back sooner than the stated maturity, extension risk, the opposite of prepayment risk, market and interest rate risk.

__________________________________________________________________________________________________________________________________________

This research material has been prepared by LPL Financial.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial is not an affiliate of and makes no representation with respect to such entity.

Not FDIC/NCUA Insured | Not Bank/Credit Union Guaranteed | May Lose Value | Not Guaranteed by any Government Agency | Not a Bank/Credit Union Deposit

Member FINRA/SIPC

RES 4054 0113

Tracking #1-137281 (Exp. 01/14)

__________________________________________________________________________________________________________________________________________

Stay Connected with Us!

Leave a comment