Will the Fed announce tapering at this week’s FOMC meeting?

The Fed is unlikely to announce that it is ready to begin scaling back/tapering its bond-purchase program, known as quantitative easing (QE), at this week’s meeting. The Federal Reserve (Fed) will hold its seventh (of eight) Federal Open Market Committee (FOMC) meetings this year on Tuesday and Wednesday, October 29 and 30, 2013.

Why is the Fed not likely to taper at this week’s FOMC meeting?

The main reason is the lack of visibility on the economy for Fed policymakers, due largely to the 16-day government shutdown that ended in mid-October 2013. The shutdown delayed a large number of crucial economic reports that Fed policymakers would like to have seen prior to this week’s meeting. In addition, the data that have been released since the September 17 – 18 FOMC meeting have generally been disappointing relative to expectations.

How has the economy evolved since the last FOMC meeting in mid-September 2013?

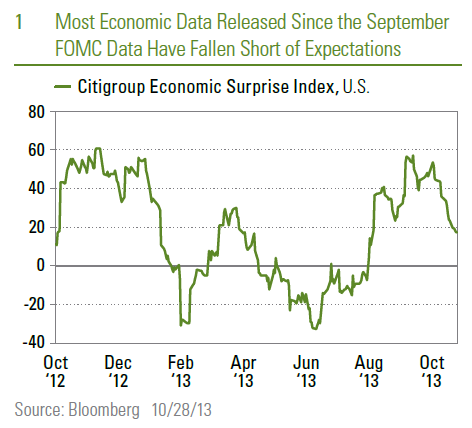

Figure 1 shows the Citigroup Economic Surprise Index for the United States over the past 12 months. The index measures data surprises relative to market expectations. A rising line means that data releases have been stronger than expected, and a falling line means that data releases have been worse than expected. The recent peak in the index came in early September 2013, just prior to the mid-September FOMC meeting. The reports released since mid-September that have fallen short of expectations include:

-

Housing starts (August)

- Richmond Fed Index (September)

- Consumer Confidence (September)

- Durable goods orders and shipments (September)

- Pending home sales (August)

- Markit PMI – Manufacturing (September)

- Vehicle sales (September)

- ISM – Non-Manufacturing (September)

- Small Business Sentiment Index (September)

- Empire State Manufacturing Index (October)

- Existing home sales (September)

- Payroll employment (September)

- Markit PMI – Manufacturing (October)

- Durable goods orders and shipments (October)

How have financial conditions changed since the last FOMC meeting?

The Fed cited tightening financial conditions as one of the reasons it chose not to begin tapering at the September 17 – 18, 2013 FOMC meeting. Figure 2 shows financial conditions – as measured by the Federal Reserve Bank of Chicago’s Financial Conditions Index — have eased since the September FOMC meeting, after tightening over the spring and summer of 2013. Note that despite tightening financial conditions between May and September 2013, they never even got close to where they were during the 2007 – 2009 financial crisis.

Will the FOMC specifically mention the government shutdown in its statement?

There is a strong likelihood that the FOMC statement will mention the recent government shutdown, and the minutes of this week’s FOMC meeting — due out in mid-November 2013 — will almost certainly mention it. The statements released during and just after the 21-day government shutdown in December 1995 and January 1996 did not specifically mention the shutdown, but in those days, FOMC statements were not as verbose as they are today. However, a quick look at the minutes from the December 19, 1995 and January 30 – 31, 1996 meetings finds that both sets of minutes did mention the shutdown and its impact on the economy. The minutes of the January 31, 1996 meeting mentioned the shutdown’s impact on the availability of economic data.

Excerpt from the minutes of the December 19, 1995 FOMC meeting:

The decline in federal purchases in part represented the transitory effects of government shutdowns and the restraining effects of spending cuts imposed by continuing resolutions and by curtailed appropriations in bills that already had been enacted into law.

Excerpts from the minutes of the January 30 – 31, 1996 FOMC meeting:

Only a limited amount of new information was available for this meeting because of delays in government releases…

…these buildups, together with the disruptions from government shutdowns…

The weakness in business activity this winter was to some extent the result of the partial shutdown of the federal government…

What else will we hear from the FOMC this week?

The only communication from the Fed at the conclusion of the meeting will be the FOMC statement, which will be released at 2 PM ET on Wednesday, October 30, 2013. There will be no new economic and interest rate forecast from members of the FOMC, nor will Fed Chairman Ben Bernanke hold a press conference. Market participants will have to wait until the conclusion of the December 17 – 18, 2013 FOMC meeting for the next economic and interest rate forecasts from the FOMC. The press conference following that meeting will be Ben Bernanke’s last as Fed Chairman. We expect that in the near future, the FOMC will strongly consider holding a press conference at each of its eight meetings per year. Many other major central banks across the globe hold press conferences and release forecasts at the conclusion of all of their meetings. In addition, most global central banks hold meetings once a month.

It’s nearly two months away, but what about the next FOMC meeting (December 17 – 18)?

As we noted in last week’s (October 21, 2013) Weekly Economic Commentary: The Lowdown on the Shutdown — The Impact on the Economy and the Fed, the 16-day government shutdown caused delays in the government’s data collection and reporting process for economic data. Since the government’s economic data calendar will not be back to normal until early December, it is unlikely Fed policymakers will announce tapering at the December 17 – 18 FOMC meeting.

An additional hurdle to tapering is the timing of the next government shutdown and debt ceiling debate. Under the terms of the bill passed by Congress in mid-October 2013 to end the shutdown and lift the debt ceiling, the government could shut down again in mid-January 2014, and the Treasury could hit its borrowing limit by early February 2014. While we see this as unlikely, as has been the case in the past few years,these deadlines create uncertainty for the public, market participants, and policymakers and could weigh on economic activity.

In addition, a special bipartisan House-Senate conference committee charged with breaking the impasse on the budget is scheduled to issue a report on December 13, 2013, just days before the December 17 – 18, 2013 FOMC meeting. While a “grand bargain” on the budget might pave the way for the Fed to taper in December 2013, the more likely outcome is that the rancor surrounding this report will only add to the fiscal uncertainty, which argues for a Fed taper in early 2014 and not at the December 17 – 18, 2013 meeting. Of course, if Congress can agree in the next few weeks (for example, by Thanksgiving) on a deal that would eliminate the possibility of another shutdown and bruising debate about the debt ceiling in early 2014, a December taper becomes more likely.

______________________________________________________________________________________________________________________________

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance reference is historical and is no guarantee of future results. All indices are unmanaged and cannot be invested into directly.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Stock investing involves risk including loss of principal.

Quantitative easing is a government monetary policy occasionally used to increase the money supply by buying government securities or other securities from the market. Quantitative easing increases the money supply by flooding financial institutions with capital in an effort to promote increased lending and liquidity.

The Federal Open Market Committee (FOMC), a committee within the Federal Reserve System, is charged under the United States law with overseeing the nation’s open market operations (i.e., the Fed’s buying and selling of U.S. Treasury securities).

______________________________________________________________________________________________________________________________

INDEX DESCRIPTIONS

Citigroup Economic Surprise Index (CESI) measures the variation in the gap between the expectations and the real economic data.

The National Financial Conditions Index (NFCI) measures risk, liquidity and leverage in money markets and debt and equity markets as well as in the traditional and “shadow” banking systems. Positive values of the NFCI indicate financial conditions that are tighter than average, while negative values indicate financial conditions that are looser than average.

___________________________________________________________________________________________________________________

This research material has been prepared by LPL Financial.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial is not an affiliate of and makes no representation with respect to such entity.

Not FDIC/NCUA Insured | Not Bank/Credit Union Guaranteed | May Lose Value | Not Guaranteed by any Government Agency | Not a Bank/Credit Union Deposit

Member FINRA/SIPC

Leave a comment