In 2014, interest rates are likely to continue to move higher and bond prices lower in response to improving economic growth, reduced Federal Reserve (Fed) bond purchases, and the likelihood of an interest rate hike in 2015. Even though a Fed rate hike is a 2015 event, bond prices are likely to decline and yields increase as valuations remain expensive to historical averages and forward-looking markets prepare for a rate hike. We view the start of interest rate hikes as more important than the pace of tapering, but tapering will mark the first step in bond prices and yields returning to historical norms. We see a defensive investment posture focused on less interest rate sensitive sectors as the most prudent way to invest in 2014.

Yielding to Growth

Longer-term bond yields have historically tended to track the change in gross domestic product (GDP) growth absent the influence of Fed actions. Our expectation for a 1% acceleration in U.S. GDP over the pace of 2013 suggests a similar move for the bond market. This would prompt a rise in the yield on the 10-year Treasury from around 2.75% as of mid-November 2013 to about 3.25% to 3.75% in 2014.

On the Horizon

While investors may see the Fed end direct involvement in the bond market in 2014 as the bond-buying program comes to a close, the Fed may make its presence felt again in 2015 with a series of rate hikes. The expectation for rate hikes in 2015 may also lead to rising pressure on bond yields in 2014. Each period of Fed interest rate hikes is different, but by evaluating key metrics such as short-term Treasury yields, the shape of the yield curve, and inflation-adjusted yields prevalent at the start of prior Fed rate hikes, we can approximate the trajectory of yields in 2014 as the market braces for a potential interest rate hike in 2015.

Given the Fed’s current guidance for a mid-2015 start to interest rate hikes, supported by our outlook for stronger GDP and job growth in 2014, we may expect at least an 18-month path of reduced Fed involvement in the bond market from around the start of 2014 to mid-2015. This reinforces the fundamental case for the 10-year Treasury yield rising by 0.5% to 1.0% as yields rise to more “normal” valuation levels that would translate to a 10-year Treasury yield at the end of 2014 of 3.25% to 3.75%. Total returns may be roughly flat under that scenario [Figure 1].

It is possible that yields could increase by 1.0% to 3.75% should inflation-adjusted yields return to more normal levels. Under that scenario, high-quality bond total returns would be negative, as indicated by Figure 1. However, we see a move of this magnitude as less likely unless the markets expect an earlier start to Fed rate hikes. Instead, we think it is more likely the Fed may wait longer than mid-2015 to raise interest rates, which supports a more modest rise in the 10-year of 0.50% to 0.75%.

A number of factors indicate yields may rise less than our forecasts, and this is the primary risk to our bond outlook.

-

Low Inflation. Inflation is an enemy of bondholders since it makes fixed payments worth less over time. While inflation is likely to pick up modestly in 2014, fortunately, it is likely to remain historically low. Bond valuations may therefore remain historically expensive. The lower the pace of inflation, the less bond yields will need to rise in response.

- Disappointing growth. Slower-than-expected growth may reinforce the low inflation environment and delay the timing of eventual Fed rate hikes — both of which are positives for bond prices. Should the economy grow at a slower pace than anticipated in 2014, bond prices may similarly prove more resilient.

- Fed delays. Our interest rate forecast is based upon the Fed gradually tapering bond purchases in 2014 and market participants’ expectation for a potential interest rate hike in June 2015. If these are pushed back, yields may rise less than our base forecast and bond prices may prove more resilient. Low single-digit returns may result if it becomes clear the Fed may wait longer than mid-2015 to raise interest rates.

Stay in the Middle

Among high-quality bonds we prefer intermediate-term bonds, which possess far less interest rate risk compared with long-term bonds [Figure 2]. The yield curve remains relatively steep today. A positive factor for intermediate-term bonds is that they include the steepest portion of the yield curve. A yield curve is a chart of bond yields from the shortest-maturity issues to the longest-maturity ones. The steepest point is that which offers the biggest increase in yield per additional increase in term.

While short-term bonds offer the least interest rate risk, their low yields make them less attractive. We believe intermediate-term bonds possess a better combination of interest rate risk mitigation and reward in the form of yield under a range of outcomes.

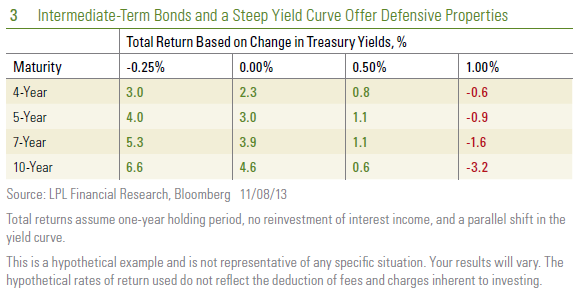

Intermediate-term bonds have the ability to generate modestly positive returns despite a fair rise in interest rates. Importantly, given their position on the yield curve, intermediate-term bonds can also provide some defensive properties to a portfolio [Figure 3]. Immediate-term, high-quality bond returns turn negative with a 1.0% rise in interest rates — just above the high end of the most likely range we expect for intermediate-term bonds in 2014. However, they can produce mid-single-digit gains if interest rates are unchanged or even decline slightly — driven by disappointing economic growth or a negative event causing investors to take a temporary defensive stance. In that event, intermediate-term bonds may provide a gain offsetting losses in the event of a stock market pullback — a key reason for holding bonds in a portfolio.

Harvesting Yield

A rising interest rate environment presents a challenge to bond market investors. Investors must seek to minimize interest rate driven losses and at the same time focus opportunistically on sectors that have traditionally produced gains during rising rate environments.

High-yield bonds and bank loans are two sectors that have historically proven resilient and often produced gains during periods of rising interest rates. In 2013, both sectors were among the leaders of bond sector performance during a year of higher interest rates.

High-yield bonds and bank loans are attractive bond sectors for 2014. Deteriorating credit quality and rising defaults are the key risks to investors in these lower-rated bonds, but we believe these risks will be manageable in 2014 as growth picks up. The global speculative default rate was a low 2.8% at the end of October 2013 — well below the historical average of 4.5%. Moody’s forecasts a low default environment to persist through 2014, a forecast we agree with given the limited number of maturing bonds in 2014. In addition to a low default environment, both high-yield bonds and bank loans remain supported by good fundamentals. Company leverage has increased over recent quarters, but the cost to service that debt remains quite manageable with interest coverage near post-recession highs.

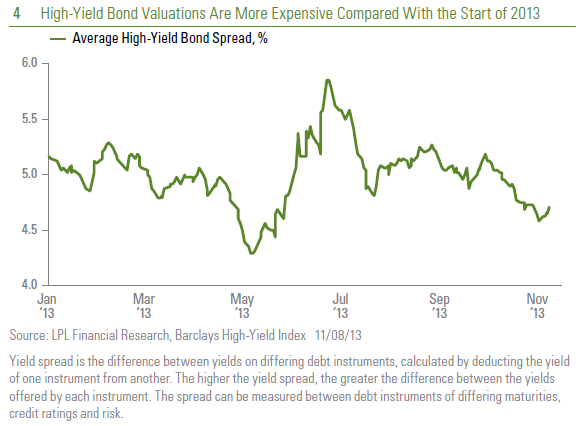

High-yield bonds and bank loans are likely to produce low- to mid-single-digit returns in 2014. High-yield bond valuations are more expensive heading into [Figure 4]. As 2014 progresses, yield spreads may increase as investors begin to demand greater compensation for a potential increase in defaults in 2015. Bank loans may also be impacted by investors bracing for higher defaults, but less than high-yield bonds due to their shorter-term nature and higher seniority.

Among high-quality bonds we favor investment-grade corporate and municipal bonds. Investment-grade corporate bonds are likely to be impacted by rising interest rates, but still yield, on average, 1.3% more than comparable Treasuries. In a rising rate environment, interest income can be a buffer against price declines associated with rising interest rates. The higher yield potential of investment-grade corporate bonds, which remain supported by good credit quality fundamentals, may therefore be able to provide better protection than Treasuries.

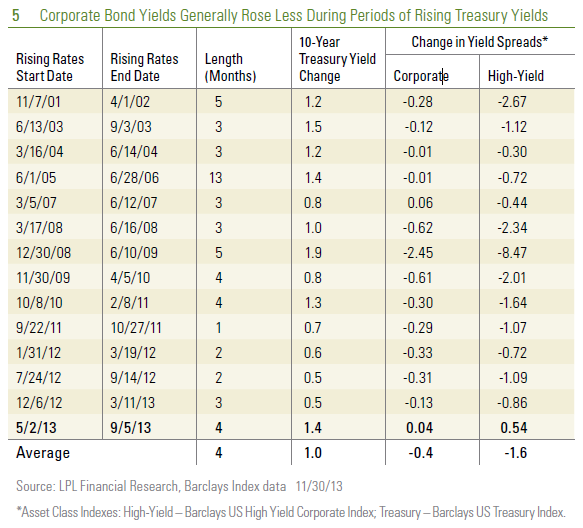

Corporate bond sectors, both investment-grade and high-yield, have historically provided better protection against rising interest rates [Figure 5]. During periods of rising Treasury yields, corporate yields tend to rise less and corporate bond prices have been more resilient. Figure 5 illustrates how the yield differential, or spread, between Treasuries and investment-grade corporate bonds and high-yield bonds has generally narrowed when Treasury yields rose. Since 2000, investment-grade corporate bond yield spreads have narrowed in all but two periods of rising Treasury yields and all but one for high-yield bonds.

Among high-quality bonds, we also find municipal bonds attractive, favoring intermediate-term rather than traditional long-term municipal bonds.

International Debt

Emerging market debt (EMD) is another way to add higher income generating potential to portfolios. In general, EMD issuers have lower debt burdens and stronger economic growth than their developed market peers. In addition, valuations are attractive as 2013 winds down with an average yield spread of 3.6% to comparable Treasuries, near the upper end of a four-year range. Better valuations set the foundation for a better 2014, following a difficult 2013. However, not all EMD issuers are alike. In the face of relatively sluggish global demand in recent years, some emerging market countries have relied on extraordinary liquidity provided by the world’s central banks to grow their economies at the cost of running current account deficits as they increasingly borrow to import more than they export. As global credit conditions tighten and developed market bond yields rise, some EMD issuers have suffered as investors find more attractive yields in more financially secure markets. As these EMD issuers adjust to the lessened liquidity provided by central banks, they become increasingly attractive. Emerging market debt is increasingly attractive in 2014, but we remain cautious on developed foreign bond markets given weak growth and unattractive valuations.

Opportunities in a Less Liquid Market

Like 2013, 2014 may also provide investors with opportunities created by volatility. In 2013, the 10-year Treasury yield fell as low as 1.6% and also rose as high as 3.0% — a remarkably wide range given the steady and sluggish pace of economic growth and lack of abrupt changes by the Fed. Although these movements may seem dramatic in a historical context, they may become the norm as recent financial regulations discourage traditional market-making firms from participating in the bond market. As a result, these less liquid markets can experience sharp swings up or down and temporarily take prices and yields beyond levels warranted by fundamentals. Tactical investors may harvest opportunities that could arise in a low-return, volatile market. This may be experienced more dramatically in less liquid markets, such as emerging market debt and municipal bonds among others.

______________________________________________________________________________________________________________________________

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results. All indexes are unmanaged and cannot be invested into directly.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values and yields will decline as interest rates rise, and bonds are subject to availability and change in price.

Gross Domestic Product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

Government bonds and Treasury bills are guaranteed by the U.S. government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value. However, the value of fund shares is not guaranteed and will fluctuate.

Treasuries are marketable, fixed-interest U.S. government debt securities. Treasury bonds make interest payments semi-annually, and the income that holders receive is only taxed at the federal level.

International and emerging market investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors.

Preferred stock investing involves risk, which may include loss of principal.

High-yield/junk bonds (grade BB or below) are not investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

International and emerging market investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors.

Preferred stock investing involves risk, which may include loss of principal.

______________________________________________________________________________________________________________________________

INDEX DESCRIPTIONS

The Barclays Capital Aggregate Bond Index is an unmanaged market capitalization-weighted index of most intermediate-term U.S. traded investment-grade, fixed rate, non-convertible and taxable bond market securities including government agency, corporate, mortgage-backed, and some foreign bonds.

The Barclays Capital High Yield Index covers the universe of publicly issued debt obligations rated below investment-grade. Bonds must be rated below investment-grade or high-yield (Ba1/BB+ or lower), by at least two of the following ratings agencies: Moody’s, S&P, Fitch. Bonds must also have at least one year to maturity, have at least $150 million in par value outstanding, and must be US dollar denominated and nonconvertible. Bonds issued by countries designated as emerging markets are excluded.

______________________________________________________________________________________________________________________________

This research material has been prepared by LPL Financial.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial is not an affiliate of and makes no representation with respect to such entity.

Not FDIC/NCUA Insured | Not Bank/Credit Union Guaranteed | May Lose Value | Not Guaranteed by any Government Agency | Not a Bank/Credit Union Deposit

Member FINRA/SIPC

Leave a comment