Bashing bank loans has become popular in recent weeks and months, but we disagree with the negative headlines. Several weeks of mutual fund outflows, following robust inflows in 2013, and liquidity concerns (i.e., the ease with which an investment can be bought or sold) highlight investor fears. Mutual fund outflows and liquidity risks are not unique to bank loans, however, and current concerns may be overblown. We continue to find the asset class one of the more attractive in the fixed income markets based on our outlook for the economy and corporate bond markets over the remainder of 2014.

Valuations suggest that bank loans have not reached the “frothy” price levels typical of overcrowded investments. Bank loans pay a floating rate of interest tied to Libor (the London Interbank Offered Rate), an overnight lending rate very similar to the target fed funds rate set by the Federal Reserve (Fed). The greater the yield advantage, or spread, that bank loans pay relative to Libor, the more attractive bank loans are and vice versa. The average spread of bank loans is approximately 4.3%, which has declined in recent years much like yield spreads across fixed income markets, but is well above the average 2.0% yield advantage that persisted prior to the financial crisis. Current yield spreads remain far away from those during the overheated market of 2006 – 07.

The average price of a bank loan is still lower today than in 2007 and has remained relatively stable near 99 in recent weeks compared with the average of just above par value (100) from late 2006 through late 2007, according to the Credit Suisse Leverage Loan Index. If bank loans were an overheated market, yield spreads and prices would likely resemble pre-crisis levels. But both metrics remain far below levels that precipitated sharp price declines.

Large leveraged buyout (LBO) transactions typified some of the excesses of the pre-financial crisis corporate bond markets. Loans issued by heavily debt-burdened companies coupled with expensive valuations led to weakness in many lower rated bonds, not just bank loans. LBO issuance has increased recently along with an improving economy that has spurred merger and acquisition activity, but as a percentage of issuance LBOs remain well below 2007 levels [Figure 1].

Refinancing still comprises the largest use of proceeds and accounts for almost 20% of new loan issuance. Refinancing is a healthy use of proceeds as it helps companies cut interest costs, which in turn can boost profitability. From 2006 to 2008, refinancing accounted for only 10% of new issuance and was behind both LBOs and outright acquisition-related loan issuance as a driver of new issuance. On a dollar volume basis LBO-related issuance exceeded $180 billion in 2007, while 2014 is on pace to finish the year near $80 billion (according to S&P LCD data as of 06/16/14) — still a stark contrast to the excesses of 2007.

The bank loan market has grown significantly in recent years, but last year’s growth was not simply due to investor mutual fund inflows. In addition to acquisitions and refinancing, a loan can be issued simply for general corporate purposes. A still low interest rate environment, a growing economy, and strong demand for floating rate debt have all fueled growth in the bank loan market. A corporate debt issuer is naturally going to be inclined to sell debt where demand is strong, and this has aided the growth of the market along with several large high profile issues. Bank loan terms can also be a viable option for companies to refinance fixed-rate debt into floating rate obligations.

Covenant Lite

The favorable terms for issuers present a longer-term risk for investors. Over 50% of loan market issues are “covenant lite” and have relaxed legal protections for investors to the benefit of issuers. By themselves relaxedprotections do not necessarily pose a problem if corporate bond markets function smoothly and demand remains steady. However, should market conditions deteriorate, weaker covenants can lead to conditions that make it easier for a company to default. At the margin, this is a risk investors must pay attention to as it raises default risks for 2015 and beyond.

Liquidity

Bank loans are one of the few fixed income categories that have recently been subject to mutual fund outflows, raising fears that additional outflows may lead to price declines due in part to their lesser liquidity. This may be a delayed reaction to investors seeking more interest rate sensitive sectors and chasing year-to-date bond market strength, which we believe is illtimed. Reduced liquidity can be a risk in other markets such as high-yield bonds and municipal bonds. Less liquid markets can contribute to greater price declines in a pullback and played a role in 2013 bond market weakness.

Outflows in combination with heavy new issuance weighed on bank loan prices in April, but since then the market has marched higher despite continued mutual fund outflows. That is partially because mutual funds comprise roughly 25% of the market and therefore are not a dominant driver. Institutional collateralized loan obligations (CLO) represent the majority buyer at approximately 50%. CLOs are investment pools that purchase floating rate loans and repackage the securities, depending on risk, to institutional investors. Demand from CLOs has been strong and can help buffer the loan market when individual investor demand is weak.

Rising Rates

Floating rate loans benefit investors most when interest rates rise, as their interest payments ratchet higher, but the current structure of the bank loan market suggests several Fed rate hikes may be necessary before interest income increases. The use of a minimum interest rate, known as a Libor floor, averages 1.0% currently, indicating the Fed would have to increase the fed funds rate to a similar level before bank loan payments increased. Under a Fed rate hike scenario, many other bond prices would likely be pressured, so we do not view this as a negative since bank loans have no interest rate sensitivity. Current floors are boosting yields now and would still provide an attractive source of return in a rising rate environment.

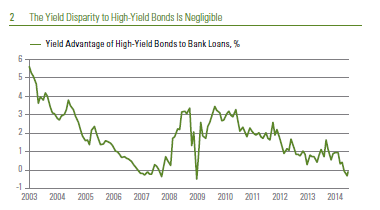

In a fixed income world with scarce opportunities, we believe bank loans could be one of the more attractive options. Demand for all types of non-Treasury securities has been robust, leaving valuations compressed across the bond market. Relative to high-yield bonds, bank loan investors have been giving up relatively little yield [Figure 2]. At the same time, high quality bonds remain expensive with yields remaining near the low end of the range, providing little room for stronger economic growth, a rise in inflation, or bearish rhetoric from this week’s Fed meeting. Although we acknowledge bank loans’ risks, we believe they are overstated and the asset class remains attractive.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance reference is historical and is no guarantee of future results. All indices are unmanaged and cannot be invested into directly. Past performance is no guarantee of future results.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Stock and mutual fund investing involves risk including loss of principal.

INDEX DESCRIPTIONS

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

Leave a comment