On Friday, the S&P 500 was up about 7% from the start of the year. This is very similar to the gains through mid-February in 2011 and 2012. These steady gains then began to be revealed as the first stage of a volatile year that frequently exhibited 5 – 15% swings in the stock market, as you can see in Figure 1.

Again in 2013, the stock market may post a gain, but those gains may be hard to discern during the course of a year that exhibits frequent swings of 5 – 15%. Fortunately, this volatility is perfectly normal.

The investing environment may be like that of 1994 and 2004, the last two times the economy experienced a transition in Federal Reserve (Fed) policy. Both 1994 and 2004 had multiple 5 – 15% pullbacks in the S&P 500 as the recovery matured, stimulus faded, and the Fed hiked interest rates marking a return to normal conditions. Both years also provided only single-digit buy-and-hold returns. Yet neither year marked the end of the bull market.

Just as in 1994 and 2004, market participants are likely to remain focused on the Fed over the coming two weeks. First, this week the Fed releases the minutes to their January meeting, providing more detail on the deliberations. Second, next week (February 26 – 27) Fed Chairman Ben Bernanke will deliver his semi-annual report on the economy and interest rates to House and Senate panels.

A key contributor to the volatility in 1994 and 2004 was the normalization of monetary policy — or, in other words, hikes to the federal funds rate by the Fed. The volatility began early in those years as the Fed signaled the coming of the rate hikes that took place later in the year. While a rate hike remains a year or two away at the earliest, the Fed is likely to begin to slow or stop the current bond-buying program, known as quantitative easing, later this year or very early in 2014. The Fed will likely note that this change in policy marks a “normalization” after providing exceptional liquidity since late 2008. Regardless of the Fed’s description, these steps toward a return to a more normal monetary environment are likely to lead to higher interest rates and tighter credit conditions for borrowers, even without the hikes to the federal funds rate that can weigh on the stock market.

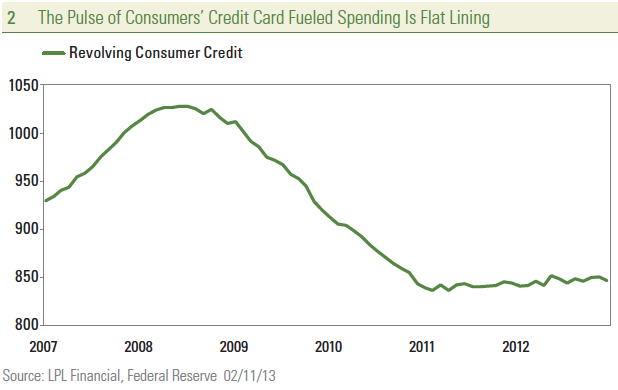

Changes to Fed programs — or even deliberations months ahead of the potential end of a program or start of a new one — have punctuated the volatile moves in the market over the past five years, as you can see in Figure 2. The coming weeks could begin to reintroduce some Fed-related volatility to the markets if the Fed signals any potential upcoming actions. However, pronounced moves are more likely to come later in the year as the Fed is closer to a change in policy.

It is relatively easy to figure out how to invest when you believe the market is likely to go up or go down, but how do you invest when it is likely to go both up AND down? There are several potential ways to benefit from market volatility, including:

- Rebalance tactically – More frequent rebalancing and tactical adjustments to portfolios are recommended to take advantage of the opportunities created by the pullbacks and rallies. Seeking undervalued opportunities and taking profits are key elements of a successful volatility strategy.

- Seek yield – Focusing on the yield of an investment rather than solely on price appreciation can help enhance total returns. Bank loans and even alternative vehicles like master limited partnerships (MLPs) offer a potential yield advantage over investments that are solely price-driven during periods of high volatility.

- Go active – Using active management rather than passive indexing strategies to enhance returns. In general, active managers tend to outperform their indexes when volatility rises, according to LPL Financial Research analysis. Opportunistic-style investments provide a wide range of opportunities for managers to exploit during volatile markets.

- Think alternatively – Increase diversification by adding low-correlation investments and incorporating non-traditional strategies that aim to provide downside protection, risk management, and may benefit from an environment of increased volatility. This would include exposure to covered calls, managed futures, global macro, long/short, market neutral, and absolute return strategies.

Some investors are wary of this volatility and view it as a sign of a fragile market. We see volatility as a normal, and even potentially rewarding, part of the investing environment for those who know how to invest for volatility.

________________________________________________________________________________________

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance reference is historical and is no guarantee of future results. All indices are unmanaged and cannot be invested into directly.

Stock investing involves risk, including the risk of loss.

Correlation is a statistical measure of how two securities move in relation to each other. Correlations are used in advanced portfolio management.

Quantitative easing is a government monetary policy occasionally used to increase the money supply by buying government securities or other securities from the market. Quantitative easing increases the money supply by flooding financial institutions with capital in an effort to promote increased lending and liquidity.

Bank loans are loans issued by below investment-grade companies for short-term funding purposes with higher yield than short-term debt and involve risk.

Master limited partnership (MLP) is a type of limited partnership that is publicly traded. There are two types of partners in this type of partnership: The limited partner is the person or group that provides the capital to the MLP and receives periodic income distributions from the MLP’s cash flow, whereas the general partner is the party responsible for managing the MLP’s affairs and receives compensation that is linked to the performance of the venture.

Federal Funds Rate is the interest rate at which a depository institution lends immediately available funds (balances at the Federal Reserve) to another depository institution overnight.

Operation Twist is the name given to a Federal Reserve monetary policy operation that involves the purchase and sale of bonds. “Operation Twist” describes a monetary process where the Fed buys and sells short-term and long-term bonds depending on their objective.

Yield is the income return on an investment. This refers to the interest or dividends received from a security and is usually expressed annually as a percentage based on the investment’s cost, its current market value or its face value.

Alternative investments may not be suitable for all investors and involve special risks such as leveraging the investment, potential adverse market forces, regulatory changes and potentially illiquidity. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk.

________________________________________________________________________________________

INDEX DEFINITIONS

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

________________________________________________________________________________________

This research material has been prepared by LPL Financial.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial is not an affiliate of and makes no representation with respect to such entity.

Not FDIC or NCUA/NCUSIF Insured | No Bank or Credit Union Guarantee | May Lose Value | Not Guaranteed by any Government Agency | Not a Bank/Credit Union Deposit

Member FINRA/SIP

________________________________________________________________________________________

Stay Connected with Us!