It was 1964, 50 years ago, that the film Goldfinger debuted. It is the quintessential James Bond film and the first one to win an Academy Award. In Goldfinger, Q — the head of the gadget-making “Q-Branch” — presents Bond an alternative to the traditional car. It can emit an oil slick and has a battering ram, a pop-up rear bulletproof screen, and even an ejector seat. These gadgets helped Bond make the best of some risky situations. Now, 50 years later, bonds are facing a risky situation — and alternative investments may help to make the best of it.

Although not part of the overall bond market measured by the Barclays Capital Aggregate Bond Index, the high-yield and municipal bonds we favor for 2014 are considered traditional investments. As your “Q-Branch,” LPL Financial Research would like to present you with some alternatives to traditional investments that may be helpful in 2014 as faster growth may lead to higher interest rates and flat returns for the bond market: bank loans, business development companies (BDCs), real estate investment trusts (REITs), and master limited partnerships (MLPs).

-

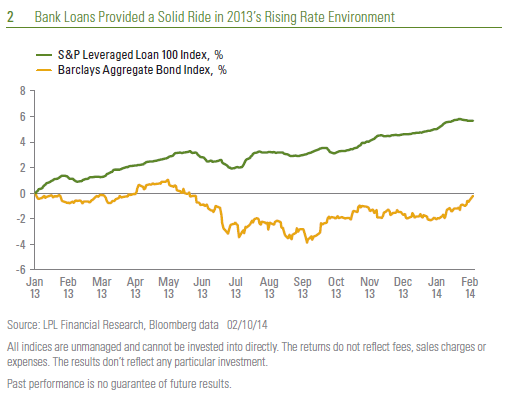

Bank loans. Bank loans are an alternative that seeks to offer an attractive yield and less interest rate risk for 2014. The interest rates on these loans made to businesses float higher with short-term interest rates. While bank loans can suffer losses when economic growth deteriorates and negatively impacts the ability of companies to repay their borrowings, we expect solid economic growth in 2014. Finally, they behaved well in last year’s interest rate run-up from May to July, as you can see in Figure 2.

-

BDCs. Business development companies function like banks by lending money to businesses. BDCs have flexibility to go beyond the most senior structured loans, so they can have more credit risk if the economy deteriorates, resulting in companies being unable to repay their debts. Illustrating this heightened leverage and credit exposure, the Wells Fargo BDC Index has behaved like 2.25 times the Barclays Capital High Yield Bond Index, as you can see in Figure 3. It is a good idea to keep the 2.25 factor in mind when considering weighting and overall portfolio credit exposure. \

- REITs. Looking back over the past 20 years, REITs (measured by the NAREIT Index) have generally provided solid yields and strong total returns with the exception of poor relative returns in 1998 – 99, 2007 – 08, and 2013. In 2013, REIT returns were similar in magnitude to 2002 and 1994, when they outperformed stocks and bonds, but in 2013 the S&P 500 Index outperformed REITs by a margin of about 30 percentage points. In 2007 – 08, credit conditions and the bursting of a real estate bubble were the problems contributing to REIT losses — something we do not expect to see in 2014. However, in 1998 – 99 and in 2013, we saw rising interest rates and a move by the Federal Reserve to become less bond market friendly. We expect that to be the case in 2014 as well. In 2013, interest rates went up in the late spring and early summer without being accompanied by better economic growth and that led to poor returns for REITs and remains a risk for 2014. However, in 2014 we expect better growth to accompany the rise in rates — making a better environment for REITs as occupancy and rents rise. From a valuation perspective, REITs are fairly valued on historical metrics like discount to net asset value, price to funds from operations, and spreads to BBB bonds. While they may fare better in 2014 than in 2013, REITs still face headwinds from rising interest rates, making REITs likely to underperform stocks, but outperform bonds.

-

MLPs. In comparison to REITs, rising U.S. liquid fuel transportation needs may make MLPs that operate pipelines able to re-price rents and keep up with rising rates in 2014. A key beneficiary of the American energy renaissance, pipelines are seeing strong volume growth. In 2013, MLPs provided solid mid-single digit yields and posted double-digit total returns that nearly kept up with the soaring stock market (the Alerian MLP Index produced a total return of 27.6% in 2013, less than 5% below the 32.4% for the S&P 500). The U.S. Energy Information Agency forecasts transportation of U.S. crude oil production will continue to grow in 2014 near last year’s growth rate of 16%. Rising transportation demand may help to support another year of solid performance for MLPs in 2014 despite the risk posed by higher interest rates and some degree of commodity price sensitivity.

The alternative features installed in his car that helped to make Bond safer were not safety equipment. But used in the right way, they did help to protect him and provided an advantage when facing certain risky situations. The alternative investments featured here are not safer investments. But, used the right way, they may provide some protection from the risks and the potential to capitalize on the opportunities we believe investors face in 2014.

_____________________________________________________________________________________________________________________________

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance reference is historical and is no guarantee of future results. All indices are unmanaged and cannot be invested into directly. Unmanaged index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investment. Past performance is no guarantee of future results.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Stock and mutual fund investing involves risk including loss of principal.

High yield/junk bonds (grade BB or below) are not investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

_____________________________________________________________________________________________________________________________

INDEX DESCRIPTIONS

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The S&P/LSTA U.S. Leveraged Loan 100 Index is designed to reflect the largest facilities in the leveraged loan market. It mirrors the market-weighted performance of the largest institutional leveraged loans based upon market weightings, spreads, and interest payments. The index consists of 100 loan facilities drawn from a larger benchmark, the S&P/LSTA (Loan Syndications and Trading Association) Leveraged Loan Index (LLI).

The Barclays Aggregate Bond Index represents securities that are SEC-registered, taxable, and dollar denominated. The index covers the U.S. investment-grade fixed rate bond market, with index components for government and corporate securities, mortgage pass-through securities, and asset-backed securities.

The Wells Fargo BDC Index is a float adjusted, capitalization-weighted Index that is intended to measure the performance of all Business Development Companies that are listed on the New York Stock Exchange or NASDAQ and satisfy specified market capitalization and other eligibility requirements. To qualify as a BDC, the company must be registered with the Securities and Exchange Commission and have elected to be regulated as a BDC under the Investment Company Act of 1940.

The Barclays Capital High Yield Index covers the universe of publicly issued debt obligations rated below investment grade. Bonds must be rated below investment-grade or high-yield (Ba1/BB+ or lower), by at least two of the following ratings agencies: Moody’s, S&P, and Fitch. Bonds must also have at least one year to maturity, have at least $150 million in par value outstanding, and must be US dollar denominated and non-convertible. Bonds issued by countries designated as emerging markets are excluded.

______________________________________________________________________________________________________________________________

This research material has been prepared by LPL Financial.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial is not an affiliate of and makes no representation with respect to such entity.

Not FDIC or NCUA/NCUSIF Insured | No Bank or Credit Union Guarantee | May Lose Value | Not Guaranteed by any Government Agency | Not a Bank/Credit Union Deposit

Member FINRA/SIPC