Last week’s data highlighted the growing gap between the health of businesses and consumers that is starting to contribute to a widening gap in the performance of consumer and business-driven stocks, as well.

The economic reports released last week covering the time period of January and February 2013 for orders of equipment by businesses and manufacturing activity point to strengthening business demand (new orders surged). This may not be surprising, given that corporate profits have risen to record highs and companies are sitting on lots of cash.

On the other hand, the economic data released on consumer spending was weak (2% annual growth adjusted for inflation) and reflected no acceleration over the past year, and earnings reports from big retailers (such as Wal-mart and Target) reflected lackluster consumer demand.* This may be not be any new news to some, given the well-known weak income growth and hiring in the United States keeping a lid on consumer spending power and the added drain this year from higher payroll taxes and gasoline prices.

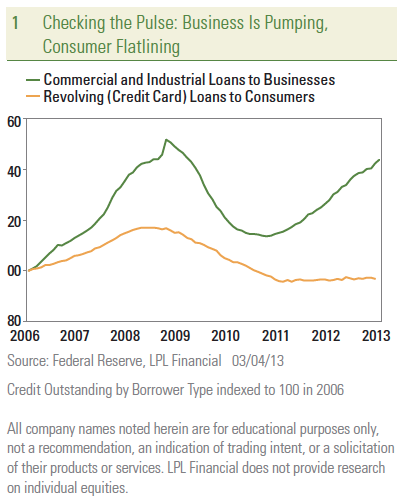

While on the subject of the last week’s data, we do not dismiss Friday’s reading of the consumer sentiment index from the University of Michigan, which showed a modest bump up in February 2013 from January 2013’s reading, but the index remains significantly below the highs of last year and is well below the pre-crisis levels seen in 2007. Sentiment surveys purport to measure how confident consumers are feeling; however, the real pulse of confidence can be measured directly by borrowing. Borrowing against the future to spend today is a sign of confidence — perhaps sometimes misplaced, but confidence nonetheless. While business borrowing has surged back near previous highs, consumers’ demand for credit has flatlined [Figure 1].

While on the subject of the last week’s data, we do not dismiss Friday’s reading of the consumer sentiment index from the University of Michigan, which showed a modest bump up in February 2013 from January 2013’s reading, but the index remains significantly below the highs of last year and is well below the pre-crisis levels seen in 2007. Sentiment surveys purport to measure how confident consumers are feeling; however, the real pulse of confidence can be measured directly by borrowing. Borrowing against the future to spend today is a sign of confidence — perhaps sometimes misplaced, but confidence nonetheless. While business borrowing has surged back near previous highs, consumers’ demand for credit has flatlined [Figure 1].

In the fourth quarter of 2012, outstanding consumer debt rose a slight 0.3% to total $11.34 trillion, according to the latest report from the Federal Reserve (Fed). But, to put in context, total debt is still way below its peak of $12.68 trillion in the third quarter of 2008 and, most importantly, has barely budged in the past couple of years. In general, consumer borrowing of all types including housing debt has been stagnant, reflecting a cautious consumer.

While in each of the past four years, consumer discretionary sector stocks outperformed the more business-spending oriented industrial sector stocks by a wide margin, they have started to lose their leadership. In the fourth quarter of 2012 and so far this year, the industrial sector has outpaced the consumer discretionary sector as business spending began to revive in the fourth quarter and gain momentum so far this year.

While in each of the past four years, consumer discretionary sector stocks outperformed the more business-spending oriented industrial sector stocks by a wide margin, they have started to lose their leadership. In the fourth quarter of 2012 and so far this year, the industrial sector has outpaced the consumer discretionary sector as business spending began to revive in the fourth quarter and gain momentum so far this year.

The next fiscal impasse is the expiration of the continuing resolution funding the government on March 27. If unavoided, this may be worse for consumers than the more recent fiscal failure to compromise over the spending cuts known as the sequester that started on Friday, March 1, 2013. As we noted in our State of the Union preview a few weeks ago, a government shutdown may hit consumers since tax refunds may take much longer than usual if IRS workers are furloughed as the seasonal peak for tax filings arrives. In 2012, the average tax refund check was nearly $3,000, and refunds totaled hundreds of billions, according to the IRS. This drag on spending power could be felt since consumers have lacked the confidence to fund spending with borrowing, as noted above. It is worth noting that the deadline is not actually March 27, because the House is in recess beginning on Thursday the 21st of March, and the Senate is only in session until the next day. Assuming Congress sticks to its schedule, this leaves only about two weeks to avoid a government shutdown and the potential consequences.

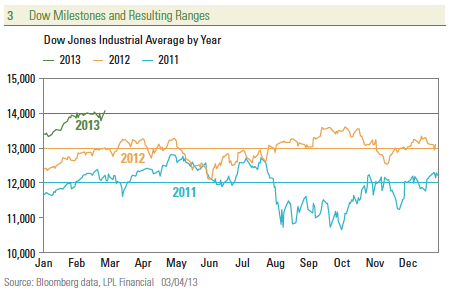

A stall in the strength of consumer-driven stocks may help to keep the stock market in a range around the current levels. Though the Dow Jones Industrial Average may soon hit an all-time high, we see this as just part of an up-and-down range-bound pattern for stocks this year, echoing what we have seen in each of the past couple of years when a new Dow milestone was reached in February [Figure 3].

A stall in the strength of consumer-driven stocks may help to keep the stock market in a range around the current levels. Though the Dow Jones Industrial Average may soon hit an all-time high, we see this as just part of an up-and-down range-bound pattern for stocks this year, echoing what we have seen in each of the past couple of years when a new Dow milestone was reached in February [Figure 3].

_______________________________________________________________________________________

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance reference is historical and is no guarantee of future results. All indices are unmanaged and cannot be invested into directly.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Stock investing involves risk, including the risk of loss.

Investments in specialized industry sectors have additional risk such as credit, regulatory, operational, business, economic and political risk which should carefully be considered before investing.

Consumer Discretionary: Companies that tend to be the most sensitive to economic cycles. Its manufacturing segment includes automotive, household durable goods, textiles and apparel, and leisure equipment. The service segment includes hotels, restaurants and other leisure facilities, media production and services, consumer retailing and services and education services.

Industrials: Companies whose businesses manufacture and distribute capital goods, including aerospace and defense, construction, engineering and building products, electrical equipment and industrial machinery. Also, companies that provide commercial services and supplies, including printing, employment, environmental and office services, or provide transportation services, including airlines, couriers, marine, road and rail, and transportation infrastructure.

_______________________________________________________________________________________

INDEX DESCRIPTIONS

Dow Jones Industrial Average (DJIA): The Dow Jones Industrial Average Index is comprised of U.S.-listed stocks of companies that produce other (non-transportation and non-utility) goods and services. The Dow Jones Industrial Averages are maintained by editors of The Wall Street Journal. While the stock selection process is somewhat subjective, a stock typically is added only if the company has an excellent reputation, demonstrates sustained growth, is of interest to a large number of investors and accurately represents the market sectors covered by the average. The Dow Jones averages are unique in that they are price weighted; therefore their component weightings are affected only by changes in the stocks’ prices.

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Michigan Consumer Sentiment Index (MCSI) is a survey of consumer confidence conducted by the University of Michigan. The MCSI uses telephone surveys to gather information on consumer expectations regarding the overall economy.

_______________________________________________________________________________________

* All company names noted herein are for educational purposes only, not a recommendation, an indication of trading intent, or a solicitation of their products or services. LPL Financial does not provide research on individual equities.

_______________________________________________________________________________________

This research material has been prepared by LPL Financial.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial is not an affiliate of and makes no representation with respect to such entity.

Not FDIC or NCUA/NCUSIF Insured | No Bank or Credit Union Guarantee | May Lose Value | Not Guaranteed by any Government Agency | Not a Bank/Credit Union Deposit

Member FINRA/SIPC

Page 3 of 3

RES 4096 0313

Tracking #1-147244 (Exp. 03/14)

_______________________________________________________________________________________

Stay Connected with Us!

www.garrettandrobinson.com

_______________________________________________________________________________________