The municipal bond market is off to its best start since 2009, when attractive valuations in the wake of the financial crisis drew robust demand. The Barclays Municipal Bond Index is up over 5% year to date through May 16, 2014 — an impressive start for any fixed income sector in just under five months — and has recouped all of the loss from the 2013 pullback plus an additional 1%.

The municipal bond market has a history of bouncing back after a tough year, and the current bounce is similar to those witnessed in recent years [Figure 1]. In 2008, volatile and illiquid bond markets led to some of the most attractive municipal valuations ever witnessed relative to Treasuries. In late 2010, fears over municipal credit quality and a default surge led to lower prices that created another buying opportunity. Two factors differentiate the 2014 rebound, which actually began in late 2013 when prices first stabilized:

Treasury market strength. Treasury prices have increased despite steady reductions in bond purchases by the Federal Reserve (Fed) and indications that the Fed remains on track to eventually raise interest rates. But sluggish economic growth during the first quarter of 2014, Ukraine-Russia tensions, emerging market growth fears, and doubts over the timing and magnitude of future Fed interest rate hikes pushed Treasury prices higher, leading to broad bond market strength in 2014 and boosting municipal bond prices in the process. The 2011 municipal rebound was also aided by stronger Treasury prices, but Treasury strength resulted from a Eurozone recession and the Fed committing to refrain from raising interest rates — a different set of drivers.

Very limited supply. Municipal bond new issuance in 2014 is running approximately 30% below the 2013 pace and is on track to be the lowest in 10 years. Higher interest rates and the limited capacity of state and local governments to take on new debt have led to a significant reduction in new municipal bond issuance, helping municipal bonds outperform Treasuries in the process.

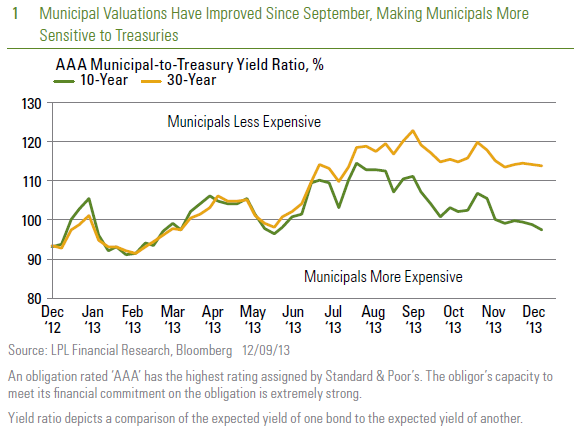

Municipal outperformance has led to more expensive valuations [Figure 2]. The average 10-year AAA-municipal-to-Treasury yield ratio still sits near a three-year low while the 30-year ratio has fallen to the lower end of its range.

On a long-term basis, municipal yield ratios remain attractive with average fully tax-exempt 30-year AAA municipal bond yields higher than comparable Treasuries. Some moderation may be likely now given the decline in yields in 2014. Average 10- and 30-year AAA municipal yields are down 1.0% and 1.1%, respectively, from 2013 peaks, and both yields are less than 0.5% above those prevalent at the start of the 2013 bond sell-off.

Caution Ahead

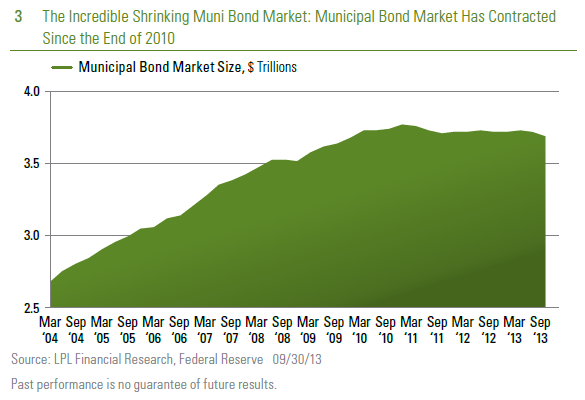

Investors are now starting to show some hesitation in response to lower yields and more expensive valuations. The amount of bonds looking to be sold, known as bid-wanteds, has increased in recent days and reflects the first signs of possible profit taking [Figure 3]. Such increases can lead to lower prices in response to rising selling pressure. Similar increases in bid-wanteds occurred in January and March of this year but were not sustained and created only minor price weakness. Also, recent increases in the amount of bonds available for sale are still below the elevated levels of 2013 that contributed to the bond pullback. The increase is therefore not a significant threat as of yet but is worth monitoring.

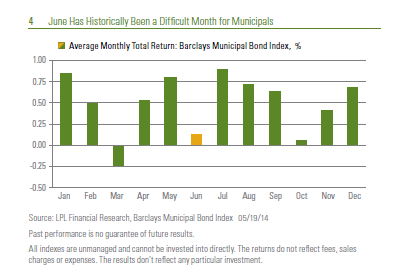

In conjunction with the first signs of selling, the month of June, especially the first half of the month, represents a difficult seasonal period for municipal bond investors as new issuance typically increases substantially.

June and July represent two of the biggest months in terms of maturing bonds, and municipalities often issue new debt to roll over maturing bonds. Caution ahead of the typical June issuance increase has historically led to

seasonal weakness for municipal bond investors [Figure 4] and it is among the weaker-performing months of performance, according to Barclays Index data. For example, the average monthly return in June has been historically only slightly positive for municipal bonds.

On a positive note, Figure 4 also illustrates that June has historically been followed by three of the strongest-performing months. Maturing bond proceeds are typically reinvested during summer months, boosting demand just as new issuance usually subsides. The seasonal summer trend did not hold in 2013, but with the limited supply trend likely to continue this year, June weakness may be limited ahead of a typically strong period for reinvestment demand. New issue supply and seasonal challenges may offset each other, perhaps posing no more than a hiccup similar to March of this year when municipal bond prices witnessed minor declines.

This leaves the taxable bond market — the other driver of strong year-to-date municipal performance — as the main catalyst for the next move in municipal bond prices, be it higher, lower, or sideways. For each rebound highlighted at the outset of this report, the direction of the Treasury market has provided a roadmap for the next significant move. Treasuries have shown remarkable resilience despite recent improvement in economic data that show a rebound in activity in the second quarter following a weather-depressed first quarter in 2014 (see Weekly Economic Commentary: Snapback, May 19, 2014). Lower Treasury yields reflect a market that needs more convincing as to the strength of the economy, but we believe the recent improvement will continue and ultimately pressure Treasury yields higher.

Absent a new bout of economic weakness, we see additional municipal price gains as limited. Prices may hang onto gains for some time, but nearterm opportunities are limited. On a longer-term basis, the favorable supply backdrop and 2013 increase in tax rates may help municipals be more resilient against the threat of rising interest rates. Over the shorter term, we continue to find the current pace of performance unsustainable, and current yields and valuations give us pause. We see recent strength as an opportunity to take gains and not as a sign of a possible buying opportunity

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance reference is historical and is no guarantee of future results. All indices are unmanaged and cannot be invested into directly. Index performance is not

indicative of the performance of any investment.

This information is not intended to be a substitute for specific individualized tax advice. We suggest that you discuss your specific tax issues with a qualified tax advisor.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values and yields will decline as interest rates rise, and bonds are subject to availability and change in price.

Government bonds and Treasury bills are guaranteed by the U.S. government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value. However, the value of fund shares is not guaranteed and will fluctuate.

Stock and mutual fund investing involves risk including loss of principal.

The Barclays Municipal Bond Index is a market capitalization-weighted index of investment-grade municipal bonds with maturities of at least one year. One cannot invest directly in an index.