The upward revision to second quarter gross domestic product (GDP) garnered a great deal of market attention last week (August 26 – 30, 2013). The report, released on Thursday, August 29, revealed that second quarter GDP — initially reported in late July 2013 as a 1.7% gain — was revised higher to a 2.5% gain. All of the upward revision to second quarter GDP can be explained by a narrower trade deficit. Initially, the trade deficit in the second quarter was reported as $451 billion, a 0.8% drag on overall GDP growth. Now, the revised data show that the trade gap stood at “only” 422 billion in the second quarter — the same as in the first quarter of 2013 — and as a result, the economic drag from trade for the quarter was eliminated. Looking ahead to the third quarter of 2013 and beyond, market participants and policymakers are asking: Can trade make a significant positive contribution to GDP growth in the quarters ahead, given the outlook for growth in Europe, China, Japan, and emerging markets?

Tracking the Pace of U.S. GDP Growth

While second quarter GDP was revised higher, the first quarter was not subject to revision and remained at 1.1%, leaving GDP growth in the first half of 2013 at a tepid 1.8%. The Federal Reserve (Fed) is still forecasting a 2.45% gain in GDP this year. With 1.8% growth in real GDP in the first half of the year, real GDP would have to grow by more than 3.0% in the third and fourth quarters of 2013 to match the Fed’s consensus forecast for the year. The Fed will release a revised forecast for the economy, labor markets, and inflation for 2013, 2014, and 2015 on September 18, 2013 at the conclusion of the next Federal Open Market Committee (FOMC) meeting. The FOMC is likely to revise downward its 2013 GDP growth forecast. The new forecast, along with the release of the FOMC’s initial public forecast for the economy, inflation, and the labor market in 2016 (also due on September 18), may help to soothe market fears about the pace of tapering and tightening.

The data in hand for the first two months of the third quarter of 2013 suggest that third quarter GDP is tracking to well under 2%, and may be closer to 1%. The data released thus far for the third quarter of 2013 include:

- Personal consumption expenditures for July;

- Industrial production for July;

- Retail sales for July and August;

- Durable goods shipments and orders for July;

- Vehicle sales for July;

- Weekly initial claims for unemployment insurance through the week ending August 24;

- ISM and regional Federal Reserve Manufacturing Indexes for July and August; and

- New and existing home sales for July.

Data due out this week (September 2 – 6, 2013) on vehicle sales, the Institute for Supply Management (ISM) Purchasing Managers’ Index (PMI), merchandise trade, construction spending, factory shipments and inventories for July and August 2013, and, of course, the August employment report (due out on Friday, September 6) will help to further clarify the pace of GDP growth in the current quarter, the rest of 2013, and into 2014.

GDP Overseas

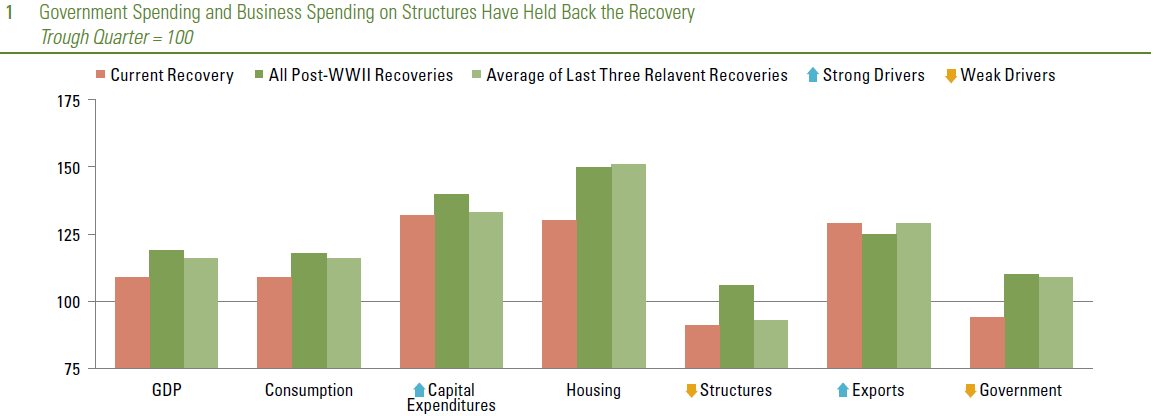

Data released over the past several months suggest that the economies in Europe and China have stabilized. Meanwhile, market participants have increased their GDP growth forecasts for Japan over the past nine months, as Japanese policymakers have ramped up monetary and fiscal policy and embarked on a series of structural reforms aimed at jarring Japan’s economy out of a multi-decade slumber. Our view remains that while the economies in China and Europe have stopped getting worse, it may take several more quarters before they can meaningfully re-accelerate. While growth has picked up in Japan — second quarter GDP growth in Japan was 2.6% — it remains disappointing relative to elevated expectations. In addition, many emerging market nations (about 50% of U.S. exports head to emerging markets), including India, Brazil, and Indonesia are now experiencing growth and inflation scares, and some (Brazil and Indonesia) are raising interest rates to head off inflation. Many of the market participants and Fed policymakers who expect U.S. GDP to accelerate in the second half of 2013 and in 2014 are likely counting on accelerating growth in Europe, China, Japan, and emerging markets to drive U.S. exports higher. But is that enough to boost U.S. GDP growth?

As noted in our Weekly Economic Commentary: Exporting Good Old American Know-How, from August 19, 2013, the United States has run a trade deficit (importing more goods and services from other countries than it exports) since the mid-1970s, and our large deficit on the goods side (around $759 billion in 2012) more than offsets the trade surplus we have on the service side of the ledger (around $213 billion in 2012). Combined, our goods and services trade deficit was $547 billion in 2012, slightly smaller than the $569 billion deficit in 2011. As a result of the slight narrowing of the deficit between 2011 and 2012, net exports contributed 0.1% to the 2.8% gain in GDP in 2012.

Net Exports Typically Do Not Boost U.S. GDP Growth

The infographic on page 2, “Profile of U.S. Exports” (Profile) reveals that over the past 40 years — aside from recessions (when imports fall faster than exports, narrowing the trade deficit) — net exports have never added more than 1.0% to overall GDP growth. Thus, even if the economies of Europe, China, Japan, and emerging markets accelerate sharply in the next few quarters, it is unlikely that net exports will provide a large boost to GDP growth this year.

In theory, an unexpected uptick in economic activity among our largest export destinations should be a plus for our exports to that region, but in practice, the impact to our trade balance and economy may not immediately reflect the better growth prospects overseas. In addition, exchange rate movements also can influence cross-border trade, but movements often work with a long lag. Since many of our exports do not compete on price, the value of the dollar is not always the best way to gauge the relative strength of our exports to many markets. Generally speaking, U.S. exports compete globally on quality, rather than price.

Export Destinations: Economic Prospects in Canada and Mexico

The Profile details the destinations (trading partners) and mix (goods versus services) of our exports. Fourteen percent of our exports (both goods and services) are bound for the Eurozone, while just 6% head to China. Remarkably, only 5% of our exports go to Japan. Combined, our exports to the Eurozone, Japan, and China account for 25% of our total exports. Closer to home, 16% of our exports head north of the border to Canada, and another 11% head south of the border to Mexico. Thus, our exports to our two closest neighbors (27% of all exports) are larger than our exports to the Eurozone, Japan, and China combined (25%). Accordingly, market participants should probably pay more attention to the economic prospects of Canada and Mexico and a bit less to the prospects of China, the Eurozone, and Japan.

Mix of Goods/Services: Goods Are 70% of All Exports

The Profile also details the goods/services mix of our exports. Currently, goods account for around 70% of all exports, but that varies widely by trading partner. The export mix to Canada and Mexico is skewed toward goods rather than services, which is partially explained by auto production, since auto parts factories and final assembly plants account for such a large portion of trade. Our export mix to the Eurozone, China, and Japan is…well… more mixed. Services, at around 40%, account for more of our trade to the Eurozone and Japan than in our overall trade mix. In China, however, an above-average 78% of our exports are goods. All else being equal, an unexpected and permanent shift higher in economic growth for trading partners like China, the Eurozone, and Japan should boost our exports to those nations over time and, in turn, our GDP. But it is important to note that outside of recessions, net exports rarely add more than 0.5% to GDP growth. So while we spend a great deal of time discussing the health of the economy in China, the Eurozone, Japan, and emerging markets, the economic prospects of our nearest neighbors (Canada and Mexico) have a bigger influence on our overall exports.

______________________________________________________________________________________________________________________________________________________________________________

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance reference is historical and is no guarantee of future results. All indices are unmanaged and cannot be invested into directly.

Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

International investing involves special risks, such as currency fluctuation and political instability, and may not be suitable for all investors.

Purchasing Managers Index (PMI) is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.

Markit is a leading, global financial information services company that provides independent data, valuations and trade processing across all asset classes in order to enhance transparency, reduce risk and improve operational efficiency. The Markit Purchasing Managers’ Index (PMIT) is a composite index based on five of the individual indexes with the following weights: New Orders – 0.3, Output – 0.25, Employment – 0.2, Suppliers’ Delivery Times – 0.15, Stocks of Items Purchased – 0.1, with the Delivery Times Index inverted so that it moves in a comparable direction.

The Institute for Supply Management (ISM) index is based on surveys of more than 300 manufacturing firms by the Institute of Supply Management. The ISM Manufacturing Index monitors employment, production inventories, new orders, and supplier deliveries. A composite diffusion index is created that monitors conditions in national manufacturing based on the data from these surveys.

Challenger, Gray & Christmas is the oldest executive outplacement firm in the United States. The firm conducts regular surveys and issues reports on the state of the economy, employment, job-seeking, layoffs, and executive compensation.

This research material has been prepared by LPL Financial.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial is not an affiliate of and makes no representation with respect to such entity.

Not FDIC/NCUA Insured | Not Bank/Credit Union Guaranteed | May Lose Value | Not Guaranteed by any Government Agency | Not a Bank/Credit Union Deposit

Member FINRA/SIPC

Health Care Checkup

October 1, 2013

What We Spend on Health Care

This week, health care is likely to be in the news as a key component of the 2010 Affordable Care Act (ACA). Enrollment for individuals seeking insurance coverage takes effect on October 1, as members of Congress continue to debate the merits (and funding) of the law as part of the discussion around providing funding for the federal government. We’ll leave the pros and cons of the ACA to the politicians and pundits and focus instead on the size and scope of the health care sector in the U.S. economy. In future Weekly Economic Commentaries, we’ll explore the impact of health care on the labor market, various segments of the economy, the federal budget, inflation, and the impact of demographics on health care spending. On balance, how we (as individuals and as an economy) consume, pay for, and manage the cost of health care will play a crucial role not only in the economy, but in the federal budget in the years and decades to come.

How We’re Covered

Most, though not all, of the spending patterns discussed below are driven by what type of health insurance, if any, individuals have. Using data compiled by the non-partisan Congressional Budget Office (CBO), which assigns people to their primary source of insurance (many people have multiple sources of insurance, especially those eligible for Medicare who also purchase additional insurance), we find that 156 million people (or 57% of the non-elderly population) have employment-based health insurance. By 2023, the CBO projects that this figure will increase to 162 million but will remain at 57% of the non-elderly population. At 57 million, or 21% of the non-elderly population, the uninsured made up the second-largest portion of the population in 2012. The CBO projects that under current law, the number of uninsured will drop to 31 million or 11% of the non-elderly population by 2023. More people are likely to move onto Medicaid and to the government-run health insurance exchanges as prescribed by the ACA while those purchasing non-group insurance will remain roughly steady at 8% of the non-elderly population. This potential shift in how Americans purchase health insurance has major implications for the overall economy and the outlook for the budget, which we’ll discuss in depth in future editions of the Weekly Economic Commentary.

How We Spend Our Health Care Dollars

Economy-wide (federal, state, and local governments, corporations, and individuals), Americans spent $2.7 trillion (or roughly 18% of gross domestic product [GDP]) on health care products, services, and investment in 2011, the latest data available.

To put that in perspective, only three countries, China, Japan, and Germany, have economies larger than $2.7 trillion. Ten years ago, the figure was closer to 15% of GDP, and 30 years ago (1982) health care represented less than 10% of GDP. The rise in the percentage of the economy accounted for by health care is because spending on health care has risen much faster than GDP. Over the last 10 years, for example, health care spending has increased at a 5.5% annualized rate while overall GDP has increased at only a 4.0% pace. Although the aging population has played a role in this increase, and will continue to for many decades to come, health care spending per capita has increased 5% per year over the past 10 years to nearly $9,000, suggesting that even without the demographic shift, we are spending more on health care than ever before.

Of the $2.7 trillion spent economy-wide on health care in 2011, about one-third is on hospital services, another 25% is on professional services (doctors, dentists, clinics), and 15% is on medical products, including pharmaceuticals, medical equipment, and medical supplies. $308 billion is spent by individuals out of pocket on health care, more than is spent by individuals on new passenger cars and light trucks (approximately $240 billion in 2012), furniture and appliances (~$275 billion), or clothing (~$290 billion). Health insurance pays for another $2 trillion in health care expenses. Private insurance covers $900 billion of that $2 trillion, Medicare insurance for the elderly covers $550 billion, and Medicaid insurance for the poor covers $400 billion. The surprise here is that out-of-pocket expenses (~$300 billion) as a percent of total health care expenditures ($2.7 trillion) are just 11%, and have been moving lower for more than five decades.

As noted above, we’ll discuss the impact of health care spending on the federal budget in a future edition of the Weekly Economic Commentary, but it’s important to note that the portion of health care spending economywide “sponsored” by governments has risen steadily over the past 25 years and is projected to continue to increase over the next 10 years and beyond, as the population ages and more people move into Medicare.

Allocation of Health Care Dollars Shifting Toward Government

In 1987, 68% of health care spending was initiated by the private sector (private businesses, households, and health-related philanthropic organizations), with one-third coming from businesses and roughly twothirds from households. Within the private sector, the ratio between businesses (one-third) and household spending (two-thirds) has remained relatively steady over the past 25 years. In 2012, just 55% of health care spending was initiated by the private sector, down from 68% in 1987, while government (federal, state, and local) accounted for 45%, up from 32% in 1987. This trend is expected to rise over the next 10 years.

Business spending in this context includes:

Household spending on health care includes:

Shifts in the mix of spending by businesses and consumers on various aspects of health care will continue to impact the economy for many years to come, and hopefully inform policy choices about who pays and how much is paid for health care in the coming decades.

Because the U.S. government is paying an ever-increasing share of health care costs, and more businesses and individuals are paying less out of pocket for health care, the actual cost and quality of health care is not as transparent as it should be. For example, we are likely to know far more about the cost and quality of the house we’re going to buy, the car we’re going to lease, and the vacation we’re going to take than we often do about our health care purchases. The overall cost of health care, combined with the lack of transparency throughout the system, will likely remain ongoing concerns for health care policymakers in the coming years and decades.

_________________________________________________________________________________________________________________________________________________________________________________

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance reference is historical and is no guarantee of future results. All indices are unmanaged and cannot be invested into directly.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Stock investing involves risk including loss of principal.

Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The Congressional Budget Office is a non-partisan arm of Congress, established in 1974, to provide Congress with non-partisan scoring of budget proposals.

This research material has been prepared by LPL Financial.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial is not an affiliate of and makes no representation with respect to such entity.

Not FDIC/NCUA Insured | Not Bank/Credit Union Guaranteed | May Lose Value | Not Guaranteed by any Government Agency | Not a Bank/Credit Union Deposit

Member FINRA/SIPC

Posted in Affordable Care Act, China, Congressional Budget Office (CBO), GDP - Gross Domestic Product, Germany, Health Care, Healthcare cost, Hospital Cost, Insurance, Japan, Medicaid, Medicare, Weekly Economic Commentary | Tagged: Affordable Care Act, CBO, China, Congress, GDP, Germany, healthcare, Healthcare costs, Hospital costs, insurance, Medical, Weekly Economic Commentary | Leave a Comment »