The ABC’s of GDP

GDP = C + I + G + (X-M)

College freshmen know it — or should know it — by the end of their Economics 101 classes, but for most of us, freshman year in college remains a bit “fuzzy” for a variety of reasons. On Friday, April 26, 2013, the Bureau of Economic Analysis (BEA) of the U.S. Department of Commerce released the first estimate of gross domestic product (GDP) for the first quarter of 2013. Inflation-adjusted, or real, GDP expanded at a 2.5% seasonally adjusted annualized rate in the first quarter of 2013, after rising at just 0.4% in the fourth quarter of 2012. The 2.5% increase fell short of expectations for 3.0% growth. Over the last three quarters (third quarter of 2012, fourth quarter of 2012, and first quarter of 2013), real GDP growth has averaged 2.0%. We continue to expect GDP growth to average around 2.0% over the course of 2013.

Although consumer spending, housing, and inventory accumulation accelerated in Q113 versus Q412 and added to growth, business spending slowed dramatically, and the trade deficit widened, dampening growth. Housing construction added 0.3 percentage points to GDP in the first quarter, marking the eighth quarter in a row that housing has added to GDP, after a five-year period (2006 – 2010) where housing was a drag on GDP.

Although consumer spending, housing, and inventory accumulation accelerated in Q113 versus Q412 and added to growth, business spending slowed dramatically, and the trade deficit widened, dampening growth. Housing construction added 0.3 percentage points to GDP in the first quarter, marking the eighth quarter in a row that housing has added to GDP, after a five-year period (2006 – 2010) where housing was a drag on GDP.

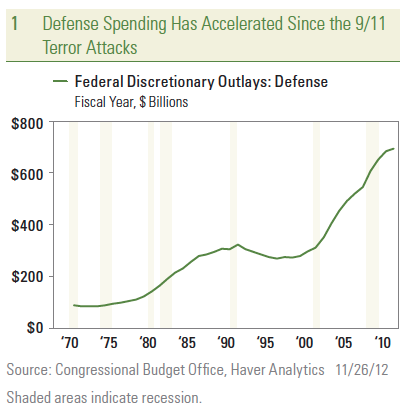

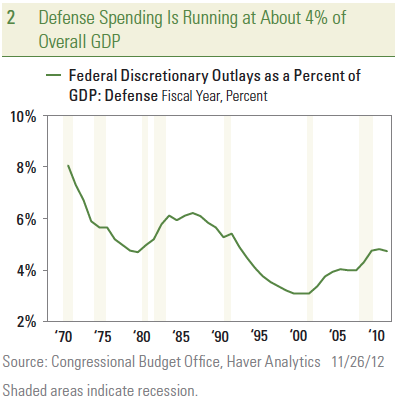

The big story in the GDP report was again federal government spending. Defense spending fell 11.5% annualized between Q412 and Q113, after the 22% drop in Q412 versus Q312, the largest back-to-back drop in defense spending in 60 years. The sequester, which cut federal government spending across the board beginning on March 1, 2013, contributed to a 2.0% drop in non-defense federal spending between Q412 and Q113. State and local government spending fell again, too, by 1.2% between Q413 and Q113, the second consecutive quarterly decline, and the 13th quarterly decline in state and local spending in the past 14 quarters, dating back to the end of 2009. On balance, there were few, if any signs, in the GDP report for the first quarter of 2013 that the economy will re-accelerate anytime soon.

The ABC’s of GDP

A – (Seasonally) adjusted. GDP is reported by the BEA in several different ways, but the most commonly cited way is on a real (inflation-adjusted) seasonally adjusted annualized basis. GDP is seasonally adjusted to smooth out the fluctuation in the economy related to weather patterns, shopping patterns, holidays, school vacations, etc., to allow apples-to-apples comparisons between quarters. For example, vehicle assembly plants typically shut down in July, which would depress GDP in the third quarter (July, August, and September) relative to the second quarter (April, May, and June). Similarly, sales of jewelry spikes around Christmas and again at Valentine’s Day. Seasonally adjusting the data helps market participants to see through the swings in the seasonal data and helps to reveal the true underlying health of the economy at any time of the year.

B – Business capital spending. Part of “I,” business capital spending (capex), is what businesses spend on machinery, software, furniture, vehicles, computers, iPads, etc. Businesses spent an annualized $1.2 trillion on equipment and software in the first quarter of 2013, accounting for 8% of GDP. Business capital spending is very sensitive to economic conditions. Business capital spending did not surpass its pre-Great Recession peak of $1.1 trillion until mid-2012. Market participants digest plenty of “input” data on business capital spending — Institute for Supply Management (ISM), durable goods orders and shipments, the regional Federal Reserve Bank manufacturing indices, reports from companies, truck sales, steel production, and rail car loadings — well ahead of the GDP report, but there is more information available to gauge consumer spending than there is to gauge business spending.

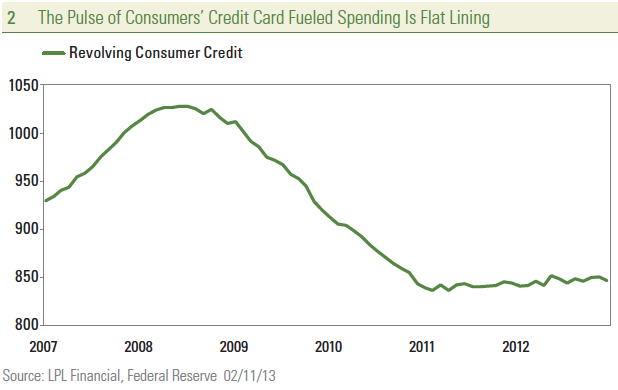

C – Consumption or consumer spending, on durable goods, non-durable goods, and services. Consumption accounts for two-thirds of GDP. In the first quarter of 2013, consumers spent an annualized $9.7 trillion, adjusted for inflation. Consumption surpassed its pre-Great Recession peak of $9.3 trillion in early 2011. Of all the categories of GDP, consumption is the most visible to most consumers. We all spend money on various items every day. The data sets that provide input to the consumption portion of GDP — weekly retail sales, chain store sales, vehicle sales, etc. — is both robust and abundant. By the time GDP is released, most market participants have a pretty good sense of what this component of GDP is doing.

D – Durable goods. Consumer spending on durable goods (items designed to last more than three years), including microwave ovens, refrigerators, and color TVs. Consumers spent an annualized $1.4 trillion on durable goods in the first quarter of 2013. Spending on durable goods surpassed the pre-Great Recession peak of $1.2 trillion in early 2011. Consumer spending on durable goods represents 15% of total consumer spending, and is the category of consumer spending that is the most sensitive to overall economic conditions.

E F

G – Government spending, including spending by the federal government and state and local governments. Governments spent an annualized $2.4 trillion in the first quarter of 2013, with the federal government spending just under $1 trillion and state and local governments spending $1.4 trillion. Government spending peaked in 2009 and 2010 at around $2.6 trillion, and since then most of the drop in government spending has been on the state and local side. Overall government spending accounts for just under 18% of GDP. Plenty of data on federal government spending are available to market participants (Daily Treasury Statement, federal employment, etc.), but little timely information is available on state and local government spending prior to the release of the quarterly GDP data.

H – Housing, which in GDP parlance, is counted as residential investment, which is captured in the “I” of our equation. Housing is counted in GDP when a new home, or condo, or multifamily apartment or dorm room is built. Housing accounts for less than 3% of GDP, and at a spend rate of just under $400 billion in the first quarter of 2013, remains at half of its pre-Great Recession spending rate of close to $800 billion hit in 2005. Both the severity of the Great Recession — and it slackluster aftermath — can be traced back to the housing market. Plenty of timely data are available on the housing market each month: new and existing home sales, various home price metrics, data on construction and housing starts; all provide market participants with a good gauge of the housing market prior to the release of the GDP data.

I – Investment, and includes business spending on equipment and software (capital spending), on structures (factories, office parks, and malls), on inventories, and consumer spending on housing.

J K L

M – Shorthand for imports. Imports subtract from GDP because U.S. businesses and consumers send money overseas in exchange for goods and services. On an annualized basis, the United States imported $2.3 trillion (annualized) of goods ($1.9 trillion) and services ($0.4 trillion) in the first quarter of 2013.

N – Nondurables. Consumer spending on nondurable goods (goods designed to last less than three years) include items like milk, motor fuel, magazines, and men’s clothing. Consumers spent an annualized $2.1 trillion on nondurable goods in the first quarter of 2013. Consumer spending on nondurable goods accounts for 21% of consumer spending, and this categoryof spending surpassed its pre-Great Recession peak in late 2010. Consumer spending on non-durables is less sensitive to economic conditions than spending on durable goods, but more sensitive than spending on services.

O P Q R

S – Services. Consumer spending on services (housing, haircuts, healthcare, hotels, etc.) is the largest category of consumer spending. Consumers spent an annualized $6.2 trillion on services in the first quarter of 2013. Consumer spending on services surpassed its pre-Great Recession peak of $6.0 trillion in early 2011. Consumer spending on services represents 64% of consumer spending, and is the category of consumer spending that is least sensitive to overall economic conditions.

T U V W

X – Shorthand for exports. Exports add to GDP because the income received by U.S. businesses from overseas in exchange for the goods produced exceeds the cost to the economy of producing the goods. Inflation-adjusted exports ran at a $1.9 trillion annualized rate in the first quarter of 2013, and surpassed their pre-Great Recession high in late 2010. Exports consist of goods exports ($1.3 trillion) and service exports ($0.6 trillion). The United States is a net importer of goods (we import more than we export), e.g., cars, jet engines, and medical equipment. However, we are a net exporter of services, such as legal services, consulting services, engineering services, and financial services.

Y Z

____________________________________________________________________________________________________________________________________

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance reference is historical and is no guarantee

of future results. All indices are unmanaged and cannot be invested into directly.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur

within a defined territory.

Stock investing involves risk including loss of principal.

____________________________________________________________________________________________________________________________________

INDEX DESCRIPTIONS

Challenger, Gray & Christmas is the oldest executive outplacement firm in the United States. The firm conducts regular surveys and issues reports on the state of the economy, employment, job-seeking, layoffs, and executive compensation.

The Consumer Price Index (CPI) is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services.

The Institute for Supply Management (ISM) index is based on surveys of more than 300 manufacturing firms by the Institute of Supply Management. The ISM Manufacturing Index monitors employment, production inventories, new orders, and supplier deliveries. A composite diffusion index is created that monitors conditions in national manufacturing based on the data from these surveys.

Purchasing Managers’ Index (PMI) is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.

The Chicago Area Purchasing Manager Index that is read on a monthly basis to gauge how manufacturing activity is performing. This index is a true snapshot of how manufacturing and corresponding businesses are performing for a given month. A reading of 50 or above is considered a positive reading. Anything below 50 is considered to indicate a decline in activity. Readings of the index have the ability to shift the day’s trading session one way or another based on the results.

The S&P/Case-Shiller U.S. National Home Price Index measures the change in value of the U.S. residential housing market. The S&P/Case-Shiller U.S. National Home Price Index tracks the growth in value of real estate by following the purchase price and resale value of homes that have undergone a minimum of two arm’s-length transactions. The index is named for its creators, Karl Case and Robert Shiller.

____________________________________________________________________________________________________________________________________

This research material has been prepared by LPL Financial.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial is not an affiliate of and makes no representation with respect to such entity.

Not FDIC/NCUA Insured | Not Bank/Credit Union Guaranteed | May Lose Value | Not Guaranteed by any Government Agency | Not a Bank/Credit Union Deposit

Member FINRA/SIPC