Municipal bond investors may face another challenging year in 2014, as we believe yields are likely to continue to move higher and bond prices lower. In most cases, we expect flat to marginally positive returns as interest income offsets price declines, but losses are likely if yields rise to the high end of our forecast. Similar to our outlook for the taxable bond market, we expect municipal yields to move higher by 0.3% to 0.8% compared to our outlook of a 0.5% to 1.0% increase for Treasuries. The smaller rise in yields compared to taxable bonds reflects our belief that municipal bonds will prove more resilient to rising interest rates in 2014 compared to Treasuries. Still, municipal bond prices will not be immune to rising interest rates in response to improving economic growth, reduced Federal Reserve (Fed) bond purchases, and the likelihood of an interest rate hike in 2015.

Early Headwinds

Municipal bond investors may face headwinds early in 2014 that may give way to potential opportunities later in the year. Three factors may contribute to early headwinds for municipal bonds.

-

A difficult seasonal period. Late February to early April marks a historically difficult seasonal period in the municipal bond market. Investors often sell municipal bonds to pay for capital gains taxes ahead of tax day, April 15. Since 2013 is shaping up to be a strong year for equity gains, tax-related selling is more likely to occur in 2014 and may pressure municipal bond prices lower.

- Lackluster demand. Mutual fund outflows continue and may linger through the start of the New Year. Mutual fund outflows alone do not necessarily lead directly to price declines or preclude an increase in bond prices. However, fund flows are reflective of individual investor demand, which comprises 75% of the municipal bond market, and the persistence of outflows indicates that overall investor demand may still be soft to start 2014.

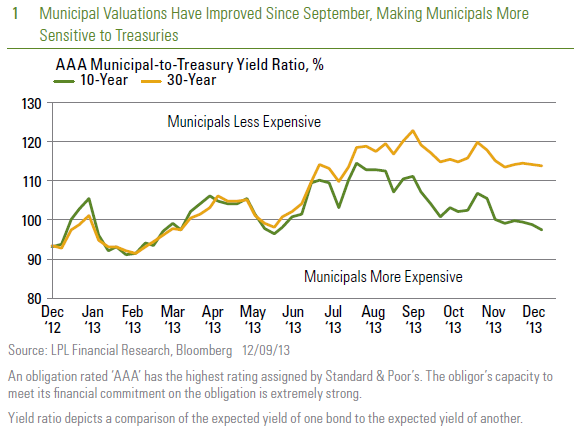

- Higher valuations. Finally, municipal bond valuations have improved over recent months relative to Treasuries. Municipal-to-Treasury yield ratios are at the lower end of a six-month range [Figure 1], even if they remain elevated on a longer-term basis. As Figure 1 illustrates, municipal-to-Treasury ratios have failed to fall further in recent months after reaching current levels, leaving municipal bonds more sensitive to Treasury price movements. While ratios are still indicative of an attractive valuation over the longer term, the combination of continued outflows and the approach of a difficult seasonal period suggests limited scope for further valuation improvement at the start of 2014 to offset any price weakness.

Tailwind Opportunities

Early weakness may give way to tailwinds and buying opportunities later in the spring and summer of 2014. In 2013, price swings were often exacerbated by illiquid markets, and creating pockets of opportunity. The same may hold true in 2014 as liquidity remains constrained. Traditional taxable bond buyers entered the municipal bond market at times to take advantage of more extreme valuations and yields at or near 5% on high-quality bonds. Strong demand for long-term municipal bonds emerge as a greater number of high-quality municipal bond yields approach 5%. The 5% yield level has often brought out buyers and may do so once again [Figure 2].

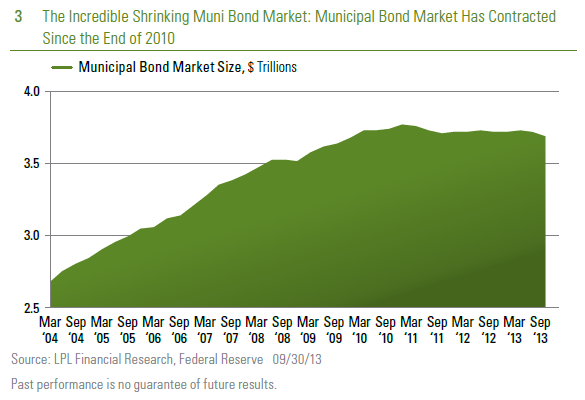

A favorable longer-term supply-demand balance failed to benefit municipal bonds in 2013 but may provide support in 2014. According to recently released Fed data, overall municipal bond market growth remains stagnant [Figure 3], and through September 2013, the market of outstanding municipal bonds is almost $90 billion smaller than its peak during the fourth quarter of 2010. The municipal market is expected to show no growth in 2014, restricting the size of the market. This favorable supply-demand dynamic may give municipal bond prices a lift once early year challenges subside.

A Modest Improvement

While 2014 may be challenging, we expect an improvement over 2013. Average high-quality municipal bond yields are closer to the 5% level now than at the start of 2013. Yields may have less room to rise, and price weakness may be more limited compared to 2013. Therefore, we expect a modest performance improvement in 2014 versus what investors are on pace to experience for 2013.

We expect high-quality municipal bond returns to be flat to marginally positive in 2014 as interest income essentially offsets price declines associated with higher interest rates. We place a lower probability on yields rising by 0.8%, the top end of our forecast, since such an increase would require the Fed to indicate an earlier start to increasing rates than their current mid-2015 guidance. We think it is more likely the Fed may wait longer than mid-2015 to raise interest rates, which supports a more modest rise in municipal bond yields of 0.3% to 0.6%. Depending on maturity, interest income may offset price declines associated with rising interest rates.

Finding the Middle Ground

We favor intermediate municipal bonds due to better protection against rising interest rates while also providing upside potential. Long-term municipal bonds, although attractively valued relative to Treasuries, present greater interest rate risk. High-yield municipal bonds may also be impacted by rising rates. Unlike taxable high-yield bonds, tax-free high-yield bonds do possess much more interest rate risk. While a diversified portfolio of municipal bonds should contain long-term and high-yield municipal bonds, we believe more attractive entry points may arise over the course of 2014, and we focus on intermediate-maturity municipal bonds.

Getting Credit

Credit quality continues to improve on a broad basis for state and local governments. State and local governments have begun to add workers for the first time in years, and the state of California is projecting a surplus for the current fiscal year for the first time in almost a decade. The improving fiscal picture should keep defaults in check. Unique situations, such as Detroit’s financial failures, are likely to remain isolated and are not representative of the broad municipal bond market. The number of defaulted issuers is on pace to finish lower for a fourth consecutive year in 2013 according to Municipal Securities Rulemaking Board (MSRB) data and is likely to remain very subdued in 2014.

Not So Taxing

The topic of tax reform will overhand the municipal market, but odds of substantive reform remain very low for 2014. In an election year, a divided Congress is once again likely to struggle to find legislation that satisfies both parties. Furthermore, both Democrats and Republicans appear to better understand the role of the municipal bond market and the lack of viable alternatives to traditional tax-exempt financing for state and local governments. Eliminating the tax exemption of municipal bond interest may fail to raise desired revenues and have negative consequences for state and local governments.

______________________________________________________________________________________________________________________________

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results. All indexes are unmanaged and cannot be invested into directly.

This information is not intended to be a substitute for specific individualized tax advice. We suggest that you discuss your specific tax issues with a qualified tax advisor.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values and yields will decline as interest rates rise, and bonds are subject to availability and change in price.

Government bonds and Treasury bills are guaranteed by the U.S. government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value. However, the value of fund shares is not guaranteed and will fluctuate.

Municipal bonds are subject to availability, price, and to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rate rise. Interest income may be subject to the alternative minimum tax. Federally tax-free but other state and local taxes may apply.

Treasuries are marketable, fixed-interest U.S. government debt securities. Treasury bonds make interest payments semi-annually, and the income that holders receive is only taxed at the federal level.

International and emerging market investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors.

High-yield/junk bonds (grade BB or below) are not investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

______________________________________________________________________________________________________________________________

INDEX DESCRIPTIONS

The Barclays Treasury index is an unmanaged index of public debt obligations of the U.S. Treasury with a remaining maturity of one year or more. The index does not include t-bills (due to the maturity constraint), zero coupon bonds (Strips), or Treasury Inflation Protected Securities (TIPS).

The Barclays Municipal Bond Index is a market capitalization-weighted index of investment-grade municipal bonds with maturities of at least one year. All indices are unmanaged and include reinvested dividends. One cannot invest directly in an index. Past performance is no guarantee of future results.

______________________________________________________________________________________________________________________________

This research material has been prepared by LPL Financial.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial is not an affiliate of and makes no representation with respect to such entity.

Not FDIC/NCUA Insured | Not Bank/Credit Union Guaranteed | May Lose Value | Not Guaranteed by any Government Agency | Not a Bank/Credit Union Deposit

Member FINRA/SIPC