Deficit Distraction

In the 12 months ending July 2013, the federal government spent $3.4 trillion and took in $2.7 trillion in revenues, making the federal deficit (revenues less spending) about $725 billion, the smallest deficit recorded since late 2008. At just 3.5%, the deficit as a percent of nominal gross domestic product (GDP) over the past 12 months was also the smallest since late 2008, and stands in sharp contrast to the 10% deficit-to-GDP ratio posted in fiscal year (FY) 2009 ending September 2009 [Figure 1].

The story is much the same fiscal year to date in FY 2013, which ends on September 30, 2013. In the first 10 months of FY 2013, the budget deficit was $607 billion, or roughly 3.6% of GDP. Outlays have totaled $2.9 trillion and revenues have totaled $2.3 trillion. The first 10 months of FY 2013 saw the smallest deficit and deficit to GDP of any comparable period back to the first 10 months of FY 2008. An improved economy, a stronger labor market, spending cuts from sequestration, and recent changes to tax rates account for most of the improvement, although a few “one-time items” have also played a role. The non-partisan Congressional Budget Office (CBO), which produces an excellent update on the progress of the federal budget every month called “Monthly Budget Review” (see http://www.cbo.gov), continues to project that the budget deficit in FY 2013 will total $642 billion, or around 4.0% of GDP.

What’s Driving the Improvement in the Deficit?

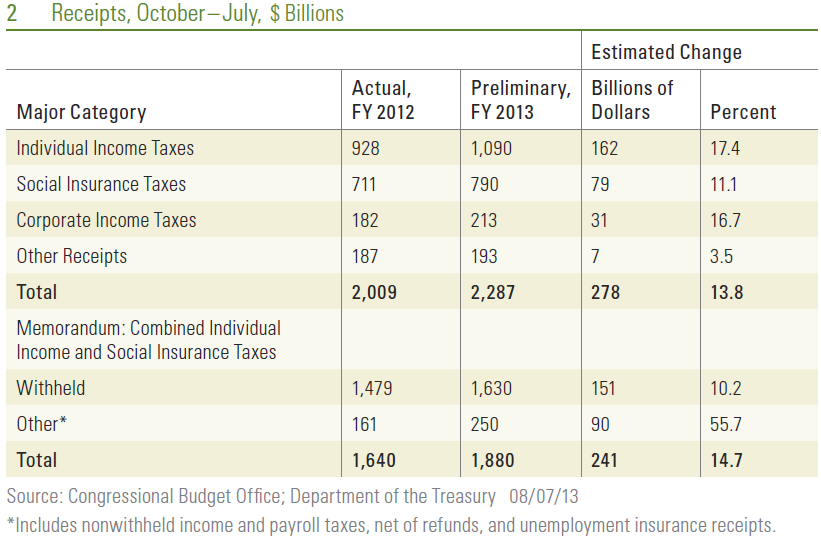

Fiscal year to date in 2013, federal revenues are up 14%, while spending is down nearly 4%. Combined individual income tax receipts — which account for around 85% of federal revenues — are up 15% in the first 10 months of FY 2013 versus the same period in FY 2012. Personal income taxes account for roughly 50% of Federal revenues while taxes withheld for Social Security and Medicare account for 35% of federal revenues. A better labor market (2.3 million net new jobs were created over the past 12 months) and rising wages (wage and salary income, as measured by the monthly report on personal income and spending, is up 4% year over year), account for some of the gain. The fiscal cliff — the expiration of the Social Security payroll tax cut in January 2013 and the increase in tax rates for incomes above certain thresholds — have also boosted revenues. The rising equity market has also accounted for some of the gain in individual tax revenues: equity markets hit new all-time highs in the first half of 2013 and investors may set aside tax payments after exercising stock options or selling stocks. Corporate profits are at record levels, and corporate tax receipts are up 17% in the first 10 months of FY 2013 versus the similar period in FY 2012. Corporate tax receipts account for 10 – 15% of federal tax revenues [Figure 2].

At $2.9 trillion, federal budget outlays in the first 10 months of FY 2013 were $90 billion (or 4%) lower than in the same period in 2012. Not surprisingly, given the solid performance of the labor market noted above, federal spending on unemployment benefits was down a whopping 24% in the first 10 months of FY 2013, while defense spending (impacted in part by the sequester) fell 7%. Federal spending activities outside of defense and entitlement programs like Social Security, Medicare, and Medicaid fell 3% in the first 10 months of FY 2013 versus the first 10 months of FY 2012, but that figure is skewed lower by payments received by the federal government from the Troubled Asset Relief Program (TARP) and big payments from the large, quasi-government mortgage giants Fannie Mae and Freddie Mac that were at the center of the financial crisis. Despite the distortions, the sequester is having a modest impact in controlling non-defense discretionary spending. Interest payments on the public debt totaled $216 billion in the first 10 months of FY 2013, down 2% from the $222 billion in the similar period of FY 2012 [Figure 3].

Warning Signs

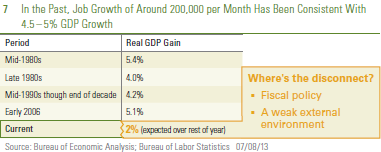

Some warning signs exist in the otherwise positive budget picture thus far in FY 2013 however, and if these warning signs continue to be ignored by policymakers, the near-term improvement in the budget picture is not likely to last. FY 2013 to date, federal spending on mandatory programs (payments set by formula written into the law) like Social Security, Medicare, and Medicaid is running above the pace of nominal GDP growth. Federal spending on Social Security benefits is up 5.4%, nearly twice the rate of nominal GDP growth over the past year (2.9%). Similarly, spending on Medicare is up 3.0% in the first 10 months of FY 2013, while Medicaid spending is up 5.7%, also about twice the rate of nominal GDP growth. The non-partisan CBO expects the improvement in the federal budget deficit to continue over the rest of this fiscal year, and for the next several fiscal years as well, through FY 2015. By then, the CBO expects the deficit as a percent of GDP to fall to 2.0%, the smallest since the 1.2% deficitto- GDP-ratio recorded in FY 2007, the last fiscal year prior to the Great Recession. From a 2.0% deficit-to-GDP ratio in FY 2015, the CBO projects that under current law, the deficit will increase to 3.2% in FY 2020 and to 3.5% by FY 2023, the last year the CBO makes a projection.

Most of the deficit deterioration in the latter half of this decade and the first half of the next occurs as a result of deterioration in the structural deficit, i.e., spending on mandatory programs like Social Security, Medicare, and Medicaid far outstripping the pace of GDP growth, mainly due to an aging population. The CBO projects that tax receipts targeted for use by those programs will only grow at the same pace as the overall economy over the next 10 years or so. Thus, the risk is that Congress and the general public will be distracted by the rapidly improving near-term budget outlook, and will not address the longer-term structural budget problem quickly enough to head off a worsening, long-term budget deficit.

____________________________________________________________________________________________________________

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance reference is historical and is no guarantee of future results. All indices are unmanaged and cannot be invested into directly.

Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

International investing involves special risks, such as currency fluctuation and political instability, and may not be suitable for all investors.

Purchasing Managers Index (PMI) is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.

Markit is a leading, global financial information services company that provides independent data, valuations and trade processing across all asset classes in order to enhance transparency, reduce risk and improve operational efficiency. The Markit Purchasing Managers’ Index (PMIT) is a composite index based on five of the individual indexes with the following weights: New Orders – 0.3, Output – 0.25, Employment – 0.2, Suppliers’ Delivery Times – 0.15, Stocks of Items Purchased – 0.1, with the Delivery Times Index inverted so that it moves in a comparable direction.

The S&P/Case-Shiller U.S. National Home Price Index measures the change in value of the U.S. residential housing market. The S&P/Chase-Shiller U.S. National Home Price Index tracks the growth in value of real estate by following the purchase price and resale value of homes that have undergone a minimum of two arm’s-length transactions. The index is named for its creators, Karl Chase and Robert Shiller.

_____________________________________________________________________________________________________________________________________________________________________________

This research material has been prepared by LPL Financial.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial is not an affiliate of and makes no representation with respect to such entity.

Not FDIC/NCUA Insured | Not Bank/Credit Union Guaranteed | May Lose Value | Not Guaranteed by any Government Agency | Not a Bank/Credit Union Deposit

Member FINRA/SIPC

Measuring Economic Expansion

August 13, 2013

The U.S. economy is now in the fifth year of the 12th economic recovery (or expansion) since the end of World War II. It is already the sixth-longest expansion and would have to last another year to become the fifth longest, as discussed in last week’s Weekly Economic Commentary: Revisiting the Recovery. This week, we will compare the performance of gross domestic product (GDP) — the broadest measure of economic activity — and its components (consumer spending, business capital spending, government spending, etc.) in the current recovery to previous economic recoveries.

Where We Stand vs. Prior Recoveries

The Great Recession of 2007 – 2009 ended in the second quarter of 2009, and the economy has been growing for 16 quarters now. Of the other 11 economic expansions since the end of WWII, just five lasted at least four years — the recoveries that began in 1961, 1975, 1982, 1991, and 2001. By the end of their fourth year in the five expansions that lasted 16 quarters or more (or “comparable recoveries”), real GDP, on average, had increased by a cumulative 19% from the end of (or trough) the prior recession. In the current expansion, the economy has grown by just 9% over the last four years (from $14.4 trillion in Q209 to $15.6 trillion in Q213) [Figure 1].

The Pace of GDP

Consumer spending, which accounts for more than two-thirds of GDP, has matched the performance of overall GDP in this expansion, growing 9% from the trough versus an average 18% gain from the trough in the other five post WWII comparable recoveries. With the exception of exports, all the other major components of GDP — business capital spending, housing, business spending on structures (office parks, malls, factories, etc.), exports and government spending — have badly underperformed the average post-WWII recovery. Why has the current recovery been so lackluster even after such a severe recession?

Several factors along with uncertainty over legislative and regulatory policy in Washington have contributed to weak growth, not only in consumption, but in all the sectors of the economy over the past four years. These factors include strained balance sheets, only modest gains in the labor market, banks’ unwillingness to lend after billions of losses in the housing bust, and a weak external environment (recession in Europe, slowdown in China, and emerging markets).

While the current expansion has lagged comparable expansions in almost every category of GDP, it may not be an “apples-to-apples” comparison. As we noted in last week’s Weekly Economic Commentary, the U.S. economy has changed significantly since the end of the inflationary 1970s. The last 30-plus years has seen the transformation of the U.S. economy from a domestically focused manufacturing economy to a more export- heavy, service-based economy. In general, this economic structure is less prone to inventory swings that drove the shorter boom-bust cycles of the past, and has led to longer expansions. On average, the last three expansions — the ones that began in 1982, 1991, and 2001 — lasted 95 months, or roughly eight years. Using those three expansions as the standard, at 49 months (16 quarters) the current economic expansion is at its midpoint, but it has been far less robust.

Using just the last three economic expansions for comparison, the pace of GDP growth in the past four years still lags the average. GDP grew by 16% over the first four years of the last three expansions, and even by that standard the current recovery (9%) is not up to par. Still, in every major category — except exports, where the current recovery matches the prior three — the current expansion falls short, in some cases far short, of the past three recoveries, especially in government spending, housing, and business investment in structures. Taking the Pulse of Government Spending Government spending in all post-WWII expansions has generally not kept pace with overall growth in GDP. Four years into the average post-WWII expansion, government spending (federal, state, and local) has increased, by 10%, about half of the increase in overall GDP (20%) [Figure2]. In the past 30 years, government spending in the first four years of expansion has increased, on average, by just 9%, lagging the overall pace of economic activity but still adding to growth. However, in the current expansion, government spending has decreased by 6%, with state and local government spending taking the biggest hit (down 8% from the second quarter of 2009). At the federal level, overall spending is down 5% from the second quarter of 2009, with an 8% cut to defense spending more than offsetting a 4% increase in non-defense spending.

Spending at the state and local level is now stabilizing, after more than five years of spending cuts. At the federal level, the impact of the sequester, the fiscal cliff, and defense cuts were still reverberating through the economy as the second half of 2013 began. On balance, government spending should be less of a drag on growth in the next four years than it was in the first four of the recovery, when government spending added to growth in only three of 16 quarters.

Taking the Pulse of the Housing Market

Although it got a late start, housing — at the epicenter of the Great Recession — has outperformed the overall economy over the past four years (as it typically does during expansions), but underperformed relative to its performance in past expansions. Housing (as measured by investment in new residential structures) has increased by 30% over the past four years, far above the 9% gain in GDP in that span. But the 30% gain pales in comparison to the 50% average gain in housing in the first four years of all post-WWII recoveries, and also falls far short of the 51% average gain in housing during the past three expansions (1982, 1991, and 2001). The hangover from the housing bust (large amounts of unsold inventory, difficulty in obtaining financing, poor consumer credit profiles, and a lackluster labor market) helps explain housing’s underwhelming performance in this recovery.

Looking ahead, our view remains that housing is in the early stages of a long recovery, aided by pent-up demand, near record-low inventories, near record-high housing affordability, a steadily improving labor market, and banks’ increased willingness to lend to borrowers. The recent rise in mortgage rates is a concern, but will likely only slow, not stop, the ongoing recovery in housing, which is being driven, in part, by cash buyers and pent-up demand.

Taking the Pulse of Business Investment in New Structures

On average, business investment in new structures (shopping malls, office buildings and office parks, factories, etc.) over the first four years of all post-WWII expansions rose 6%, lagging the pace of the average recovery in GDP (19%) [Figure 2]. Why does business investment in structures lag overall growth? In part, because these are typically very large projects with long lead times and require outsized commitments of capital, so businesses want to make sure the expansion is well entrenched before committing resources. As a result, this segment of GDP tends to lag during the early part of expansions and then picks up steam as the expansion matures. We would expect the same pattern to repeat in the current expansion.

In the three expansions since 1980, business investment on structures actually dropped by 7% over the first 16 quarters of the expansion, lagging the average of all post-WWII expansions (a 6% gain over four years). But the current expansion has seen business investment in structures fall by 9% over the past four years, an even worse performance than in the past three expansions (a 7% decrease). Business uncertainty around the health and longevity of the expansion, the turmoil in Europe and slowdown in China, as well as the legislative and regulatory backdrop, overwhelmed the positive impact of lower financing rates and years of pent-up demand. We expect business investment in structures to pick up steam and become a bigger contributor to growth in the second half of the expansion, aided by somewhat less legislative and regulatory concern and more confidence in the economy.

Taking the Pulse of Business Investment in New Structures

On average, business investment in new structures (shopping malls, office buildings and office parks, factories, etc.) over the first four years of all post-WWII expansions rose 6%, lagging the pace of the average recovery in GDP (19%) [Figure 2]. Why does business investment in structures lag overall growth? In part, because these are typically very large projects with long lead times and require outsized commitments of capital, so businesses want to make sure the expansion is well entrenched before committing resources. As a result, this segment of GDP tends to lag during the early part of expansions and then picks up steam as the expansion matures. We would expect the same pattern to repeat in the current expansion.

In the three expansions since 1980, business investment on structures actually dropped by 7% over the first 16 quarters of the expansion, lagging the average of all post-WWII expansions (a 6% gain over four years). But the current expansion has seen business investment in structures fall by 9% over the past four years, an even worse performance than in the past three expansions (a 7% decrease). Business uncertainty around the health and longevity of the expansion, the turmoil in Europe and slowdown in China, as well as the legislative and regulatory backdrop, overwhelmed the positive impact of lower financing rates and years of pent-up demand. We expect business investment in structures to pick up steam and become a bigger contributor to growth in the second half of the expansion, aided by somewhat less legislative and regulatory concern and more confidence in the economy.

Expansion Lagging Average Post-WWII Recovery

Although it is four years old, the current economic expansion has not felt like a real expansion to many consumers and businesses. Indeed, the data suggest that in virtually every segment of the economy, the current expansion has lagged the average post-WWII expansion and the three expansions since 1980, which are more comparable. While some of the factors that have weighed on the expansion are lifting, others, notably rising interest rates, are poised to take their place and we continue to expect modest (near 2.0%) growth in 2013.

______________________________________________________________________________________________________________

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance reference is historical and is no guarantee of future results. All indices are unmanaged and cannot be invested into directly.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The Federal Open Market Committee (FOMC), a committee within the Federal Reserve System, is charged under the United States law with overseeing the nation’s open market operations (i.e., the Fed’s buying and selling of United States Treasure securities).

Quantitative easing is a government monetary policy occasionally used to increase the money supply by buying government securities or other securities from the market. Quantitative easing increases the money supply by flooding financial institutions with capital in an effort to promote increased lending and liquidity.

This research material has been prepared by LPL Financial.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial is not an affiliate of and makes no representation with respect to such entity

Not FDIC/NCUA Insured | Not Bank/Credit Union Guaranteed | May Lose Value | Not Guaranteed by any Government Agency | Not a Bank/Credit Union Deposit

Member FINRA/SIPC

Posted in GDP - Gross Domestic Product, Great Recession, Homebuilders, Housing, Recovery, Weekly Economic Commentary, WWII | Tagged: GDP, Great Recession, Homebuilders, Housing, Recovery, WWII | Leave a Comment »